June’s auto market noticed plugin EVs take 35.9% share within the UK, up from 28.2% yr on yr. BEVs grew quantity 38%, and PHEVs grew 29%. Total auto quantity was 191,316 models, up some 7% YoY. The UK’s main BEV model was Tesla, with a 16.1% share of the BEV market.

June’s gross sales totals noticed mixed plugin EVs take 35.9% share within the UK, with full electrics (BEVs) taking 24.8% and plugin hybrids (PHEVs) taking 11.2%. These evaluate with June 2024 shares of 28.2% mixed, 19.0% BEV, and 9.3% PHEV.

If we put aside December months – when auto makers usually closely push BEV gross sales to fulfill full-year emissions necessities – June’s auto market truly represents a brand new report excessive in plugin share (simply forward of November ‘24). It is a good outcome, and displays the efficacy of the ZEV mandate scheme that the UK embarked upon beginning in 2024.

It additionally displays that PHEV share has just lately been as sturdy as ever, due to the brand new era of PHEVs that may sometimes drive at the least 50 miles in electric-only mode.

Lastly, it displays the truth that the month of June within the UK habitually exhibits a BEV uptick (examine the historic chart under) largely due to Tesla making a powerful end-of-Q2 push. June 2025 was no exception, with Tesla delivering 7,719 mixed models of the Mannequin Y (making it June’s third best-selling automobile general) and Mannequin 3 (sixth best-selling). This seems to be Tesla’s largest month-to-month quantity since March 2023.

In the meantime HEV share was down by some 11% YoY, petrol-only share was down by 3.5%, and diesel-only share was flat. Mixed combustion-only share stood at 51.6% and can seemingly dip under 50% by the tip of Q3.

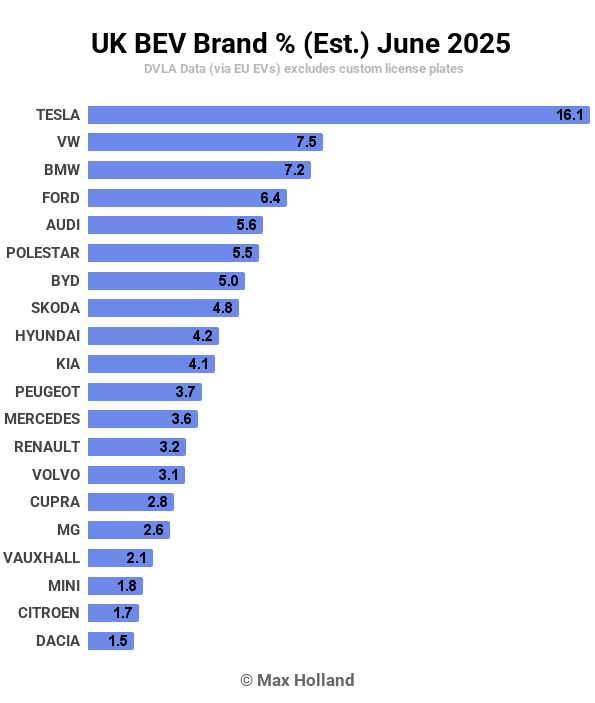

Greatest-Promoting BEV Manufacturers

As famous above, Tesla had an enormous month in June, and led the BEV model chart by a large margin, forward of the Volkswagen model, and the BMW model.

The largest mover within the month-to-month rankings was Tesla, up from 4th in Could to the highest spot in June. Most different modifications in rating had been minor shuffles, although additional again Polestar additionally jumped up, from thirteenth in Could to seventh in June.

Exterior the highest 20, the Alpine model rose from thirty seventh to twenty eighth, because of first substantial volumes (over 130 models) of its A290 mannequin. Likewise, Xpeng climbed from fortieth to thirty second, due to over 100 registrations of its G6 SUV, and the primary respectable quantity month within the UK from the revolutionary model.

As ordinary, we don’t have absolutely correct knowledge on particular person fashions (with many DVLA registrations listed as “unknown” fashions), however can pencil out some tough developments. The Skoda Elroq continued to do properly, at over 800 models in June, barely forward of its Could quantity, however under its large push in March. For context, the Elroq remains to be behind its sibling, the Enyaq (one of many high 5 with over 1000 models). It’s additionally marginally behind the BYD Seal, which noticed over 860 models in June.

On the inexpensive finish, the Dacia Spring continued to do properly, with 709 models in June, although a bit down from its 766 models in March. Its closest competitor, the Leapmotor T03 noticed 77 models in June, barely rising over its 68 models in March (each these import fashions are inclined to see peak transport quarterly). So for now Dacia has the circa-15k value section properly in hand, however extra on this under.

Stepping as much as the extra competent A-B section fashions, the Renault 5 stepped as much as its highest quantity of over 620 models in June (from a bit over 500 in Could). Which means it leads the section, forward of the Hyundai Inster, which noticed an honest 448 models in June (from 228 in Could). The Renault begins from £22,000 (40 kWh usable), while the Hyundai begins from £23,495 (39.0 kWh). Each supply bigger battery choices for extra money.

The opposite of the “legacy inexpensive trio”, the Citroën e-C3, was a way down in June with 241 models, under its March peak of 301 models. It’s too early to say whether or not that is merely a provide limitation, or a requirement limitation, but it surely’s not an ideal search for the Citroën to be at barely over a 3rd of the Renault 5’s month-to-month quantity, significantly given its barely earlier UK debut.

Renault is about to drag additional forward, with the Renault 4 simply having made its debut in June, with 51 preliminary models. As we all know, the Renault 4 shares the identical platform with – although is about 10% bigger than – the Renault 5, and has extra floor clearance. There’s no signal but of Citroën’s equal, the e-C3 Aircross.

Regardless of this seeming lead by Renault, there’s now a brand new child on the block, within the type of the BYD Dolphin Surf. Having debuted with a modest 11 models in Could, the Surf stepped as much as a major 197 models in June. It’s due to this fact already snapping on the heels of the Citroën e-C3.

The Surf is priced ranging from £18,650 for the entry (30 kWh) variant. In the meantime the Citroën e-C3’s entry £21,990 variant comes with a 44 kWh battery. Nonetheless, the entry e-C3 remains to be at an virtually similar value (per kWh of battery) because the equal Dolphin Surf, which is the 43.2 kWh “Increase” variant, with an MSRP of £21,950. So the 2 are carefully aligned when you equalise the essential specs.

When you assume this price-alignment is merely a coincidence, it’s seemingly not. One of many EU’s now under-discussion circumstances of BYD (and different Chinese language manufacturers) doing enterprise in Europe, is to have the ability to forgo tariffs in the event that they conform to undergo minimum-pricing (i.e. value fixing) to maintain European legacy auto makers blissful. Value fixing is strictly unlawful, however these anti-consumer practices ought to be no nice shock – I’ve beforehand reported on authorized findings of the cartel behaviour of Europe’s auto makers (together with their lobbies, the SMMT and ACEA).

It will be attention-grabbing to know the gross sales break up between the 2 totally different battery sizes of the BYD Dolphin Surf. The inexpensive base 30 kWh model has a modest WLTP vary of 137 miles, just like the Dacia Spring, however has rather more energy and a considerably increased high pace than the Spring (93 mph vs 78 mph), so arguably extra suited to freeway driving and all-around capacity. It additionally has quicker 10-80% DC charging (29 minutes vs 38 minutes), and a extra subtle experience, inside, and infotainment than the Spring. These benefits could justify the entry Surf’s increased value than the Spring (£18,650 vs £14,995) for some consumers.

In the meantime, the Leapmotor T03 (£15,995) has a greater WLTP vary (165 miles) than both, and comparable energy to the Surf, although a decrease high pace (81 mph) and the slowest DC charging (52 minutes for 10-80%). When you had to decide on between certainly one of these three, given their respective costs, which would it not be?

At £21,950, the mid-trim 43.2 kWh Surf is an 18% step up in value in comparison with the bottom mannequin, however has a extra helpful WLTP vary of 200 miles, the identical because the entry Citroën e-C3. There’s even a top-spec surf for £23,950 which provides extra energy and a few inside niceties, although has comparable vary. The place’s the candy spot right here? I suppose it depends upon one’s state of affairs, however tell us within the feedback.

Anyway, it’s good to see the competitors rising at these comparatively inexpensive value factors, and hopefully (except the EU and legacy auto get their means) extra fashions will shortly be a part of the fray, resulting in even higher worth for shoppers.

Right here’s the trailing 3-month chart:

Tesla’s large splash in June noticed it narrowly retake the lead over the Volkswagen model. BMW got here in third, simply forward of Ford.

This was a comparatively good outcome for Ford, which elevated its volumes 22% over Q1 and climbed from ninth to 4th. Likewise, due to the brand new Elroq, Skoda climbed from eleventh to sixth, up in quantity by 35%.

Omoda additionally climbed into the trailing-3 high 20 for the primary time, due to constant gross sales of its E5 SUV.

Outlook

The UK ZEV mandate seems to be having the supposed penalties, with the UK now pulling strongly forward of France and Germany in EV share.

The UK’s broader macroeconomy can also be marginally more healthy than its neighbours, with 2025 Q1 YoY GDP hitting 1.3% development (newest) on high of the 1.5% development from This fall. Inflation marginally cooled to three.4% in Could from 3.5% in April. Rates of interest remained on the new 4.25% fee set in early Could. Manufacturing PMI improved once more to 47.7 factors in June, from 46.4 factors in Could.

What are you anticipating from the transition within the UK? The place will EV share end the yr? Please share your ideas and views within the feedback under.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our every day publication, and observe us on Google Information!

Whether or not you’ve got solar energy or not, please full our newest solar energy survey.

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day publication for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if every day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage