“Banks are not simply monetary establishments—they’re expertise firms in disguise,” says Sharanya Ravichandran, VP of Design at JPMorgan Chase.

As digital cost strategies, cell apps, and AI-driven platforms turn into the norm, the banks that win aren’t simply these with one of the best charges or probably the most branches. They’re those that ship a unified, intuitive expertise at each touchpoint.

However right here’s the catch: whereas clients anticipate their banking to be as clean as ordering groceries on-line, many banks are nonetheless caught with siloed programs and clunky handoffs.

The end result? Annoyed clients and a rising threat of shedding them to fintech upstarts who get it proper.

Capgemini’s analysis discovered that 75% of banking clients are drawn to fintechs exactly as a result of they provide the quick, handy, and customized experiences that conventional banks battle to match.

From cell notifications to in-branch service, from digital assistants to human advisors, clients need each channel to work collectively, with out friction or repetition.

So, what precisely is omnichannel banking, how does it work, and why does it matter now greater than ever?

Let’s unpack how this method is redefining buyer expertise and what it means for the way forward for monetary providers.

Learn extra on Insider One’s Buyer engagement platform for monetary providers!

What’s omnichannel banking?

Omnichannel banking creates a seamless, linked expertise throughout all buyer touchpoints like cell apps, web sites, branches, and past.

Not like multichannel banking, the place every channel capabilities in isolation, omnichannel banking ensures that each interplay is unified and constant.

Powered by a Buyer Knowledge Platform (CDP), it permits real-time engagement, built-in insights, and a frictionless suggestions loop that drives each comfort and loyalty.

What are the advantages of omnichannel banking

Earlier than smartphones, immediate transfers, and banking apps that knew you higher than your personal accountant, what did your financial institution actually supply past a spot to deposit checks?

Nothing a lot. However within the final 5 years, retail banking has modified utterly.

Retail banks are battling for relevance in a world the place clients anticipate their monetary experiences to be as customized and frictionless.

The issue is, many retail banks are nonetheless operating on legacy programs that create fractured experiences.

A buyer would possibly begin an software in your telephone, solely to be pressured to complete it at a department.

They may contact customer support, solely to repeat your story to 3 totally different representatives.

The top result’s irritating!

However what occurs when your financial institution is aware of the shopper, understands their targets, and anticipates your wants throughout each interplay?

What occurs when you can begin an onboarding course of on WhatsApp, Fb, after which seamlessly proceed with an e-mail account setup, after which end on the app with customized banking that feels simply handy to clients?

That’s the promise of omnichannel banking, giving your clients a unified, customer-centric method that integrates each touchpoint, from cell apps to bodily branches, right into a single, seamless expertise.

Let’s discover the advantages first:

A. Enhanced buyer satisfaction and retention

Keep in mind when customized service meant your native department supervisor knew your identify?

Omnichannel banking permits retail banks to recreate that intimacy at scale, utilizing buyer knowledge to ship tailor-made recommendation, customized provides, and proactive help throughout all channels.

Think about the shopper journey as a posh, interactive story the place all touchpoints are synchronized, creating customized experiences that construct belief and loyalty.

B. Elevated operational effectivity via streamlined processes

Retail banks usually battle with fragmented programs, creating bottlenecks and inefficiencies that affect each clients and workers.

Omnichannel banking leverages cloud-based platforms and AI-powered automation to streamline processes, eradicate redundancies, and release workers to concentrate on higher-value interactions.

Zendesk’s CX Tendencies 2025 report highlights the necessity for enhancing knowledge safety, investing in new CX expertise, optimizing self-service help, and utilizing generative AI in buyer expertise, all of which align with the targets of streamlining retail banking operations.

C. Knowledge-Pushed insights for customized experiences

An omnichannel advertising and marketing method transforms the retail financial institution into a sturdy knowledge turbine, capturing real-time buyer knowledge throughout each touchpoint.

AI-powered analytics sift via this knowledge to determine traits, nuances, and patterns, enabling banks to ship hyper-personalized experiences, anticipate buyer wants, and proactively supply related services.

3 widespread challenges retail banks usually face in implementing omnichannel experiences

Based on Talkdesk’s 2024 CX in Banking survey, it’s not only a lack of channel choices that frustrates clients. A whopping 80% cited disjointed experiences when shifting throughout channels as the most important supply of frustration.

That’s like ordering a pizza on-line and having to re-enter your handle each time you name to verify on the supply.

For many retail banks, delivering this type of unified expertise is simpler stated than carried out. Siloed programs, legacy expertise, and fragmented knowledge make it robust to see the shopper as a complete individual, not only a sequence of transactions.

In the meantime, fintech challengers are elevating the bar, providing frictionless, hyper-personalized journeys that make switching banks as simple as downloading a brand new app.

So why is it so arduous for retail banks to get it proper? It boils down to 3 core challenges that flip seemingly easy buyer journeys into operational nightmares:

1. The disjointed expertise of legacy programs:

Think about making an attempt to construct a contemporary sensible residence on a basis of rotary telephones and dial-up modems. That’s what many banks are coping with.

A long time of mergers, acquisitions, and patchwork expertise upgrades have left them with a jumbled mess of core banking programs, CRM databases, and channel-specific platforms that merely don’t discuss to one another. It’s an information silo apocalypse.

2. Orchestrating the digital and bodily symphony:

Delivering a constant buyer expertise throughout digital and bodily channels isn’t nearly having a cell app and a department community.

It’s about making these two worlds work in concord. Prospects anticipate their cell app to know they simply visited a department, their telephone dialog to select up the place their chatbot session left off, and their ATM transactions to be mirrored immediately on-line.

However the actuality is commonly jarringly totally different. Siloed knowledge, inconsistent interfaces, and a scarcity of real-time synchronization can flip a easy job, like updating an handle, right into a irritating maze.

This drawback results in customers dealing with difficulties in accessing info or help as a big frustration, hurting loyalty.

3. Regulatory and safety issues:

From GDPR and CCPA to KYC and AML, retail banks function in a thicket of regulatory and safety necessities that may make even easy modifications really feel like navigating a authorized minefield.

Balancing innovation with compliance requires fixed vigilance, important funding, and a stage of experience many banks merely lack.

As AI and self-service turn into extra prevalent, the strain to guard buyer knowledge, forestall fraud, and guarantee regulatory compliance solely intensifies.

Banks should not solely undertake new applied sciences but additionally adapt their safety protocols and inside processes to safeguard towards evolving threats.

4 actionable steps you may take now to construct an omnichannel banking expertise

Up to now, you’ve understood the widespread challenges retail banks face in implementing omnichannel experiences. Now let’s be taught concerning the actionable steps you must take to beat these challenges.

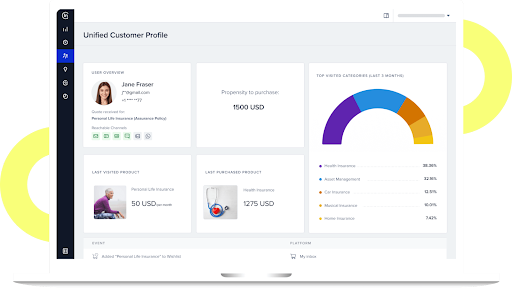

1. Combine buyer knowledge throughout channels

Each nice omnichannel expertise begins with a single supply of reality: unified buyer knowledge.

For a lot of banks, this implies investing in a sturdy Buyer Knowledge Platform (CDP) that brings collectively insights from each touchpoint—department visits, cell app exercise, name heart logs, and extra—into one 360-degree view.

Nevertheless, the issue is that conventional CDPs usually fall brief. Banks battle with gradual, advanced setups and the headache of sewing collectively a number of level options simply to activate their knowledge. The end result? Entrepreneurs bounce between platforms, workflows get tangled, and prices spiral.

The answer is a CDP that goes past storing knowledge. Insider One brings collectively 12+ activation channels, superior personalization capabilities, and a buyer journey builder below the identical umbrella as our enterprise CDP.

Moreover that, Insider One can be a pacesetter in varied classes primarily based on evaluations from clients and trade specialists.

World monetary providers supplier Allianz was trying to ship excellent experiences throughout its digital channels. Knowledge and privateness rules had beforehand prevented Allianz from gaining a holistic view of its clients to construct stronger buyer experiences. Nevertheless, Insider One’s platform enabled Allianz to gather and retailer knowledge safely and with out threat.

Insider One additionally unified the info into one dashboard, so entrepreneurs had entry to a 360-degree view of consumers throughout all touchpoints, making it simpler to create data-driven choices and enhance key outcomes.

By connecting knowledge throughout channels, Insider One enabled Allianz to construct AI-powered segments and ship buyer experiences tailor-made to every person. Allianz used this knowledge to energy an App Push marketing campaign, which achieved an 80% opt-in charge and an enormous enhance in CLTV.

Learn the complete case research right here.

2. Leverage AI to know and anticipate clients

Understanding what your clients did yesterday isn’t going to chop it anymore. The banks main the pack use AI and predictive analytics to know what their clients will need tomorrow.

You want predictive AI analytics to investigate patterns throughout hundreds of thousands of interactions to forecast wants, like when a buyer is perhaps prepared for a mortgage or susceptible to leaving for a competitor.

That’s why a superb buyer knowledge platform (CDP) like Insider One is so essential for making correct predictions. CDPs unify buyer knowledge from totally different sources into one handy database. This implies they’ll act as a central hub for storing and analyzing buyer knowledge.

Plus, our platform’s AI-powered intent engine can analyze this unified knowledge to give you correct predictions round every buyer’s chance to buy, chance to interact on a particular channel, low cost affinity, and extra.

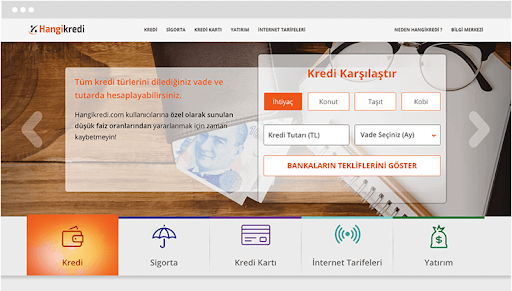

When Hangikredi used real-time analytics and AI to personalize cell mortgage functions, they made it easy for returning guests to select up the place they left off, boosting conversions by practically 7%.

Learn the complete case research right here.

3. Guarantee consistency throughout each channel

Nothing erodes belief quicker than inconsistency. Whether or not a buyer is chatting with a bot, calling help, or chatting with a teller, each interplay ought to replicate your model’s promise and data of their journey.

Fashionable journey builders and automation instruments let banks design, take a look at, and optimize buyer journeys throughout all channels.

With options like Insider One Architect, banks can orchestrate seamless transitions—so a buyer who begins a mortgage inquiry on-line can end it in-branch with out repeating themselves, and each channel looks like a part of a single, coherent dialog.

Insider One ensures you can also make each channel work collectively, so your buyer by no means looks like a stranger, regardless of the place they present up. Right here’s how:

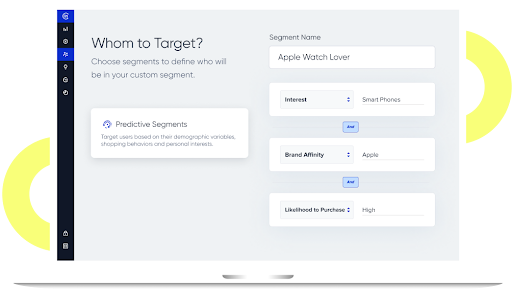

- Create AI-Powered segments: Routinely group clients primarily based on their chance to buy, most well-liked channels, or low cost affinity.

- Design dynamic journeys: Map out multi-channel experiences with a easy drag-and-drop interface, triggering customized messages primarily based on real-time behaviors.

- Check and optimize: A/B take a look at totally different messages, provides, and journey flows to repeatedly enhance engagement and ROI.

Architect offers detailed analytics at each step, permitting you to trace key metrics, determine drop-off factors, and refine your technique in actual time.

This stage of precision offers your clients a cohesive expertise throughout all of the platforms. Take Vodafone, for instance.

Vodafone was searching for methods to boost its cross-channel advertising and marketing technique and take a look at new channels to interact its viewers. They wished to extend Common Income Per Consumer (ARPU), buyer retention and loyalty, and conversions.

Insider One’s cross-channel capabilities—together with Internet Push, On-Website, E-mail, and Fb—helped Vodafone interact its viewers with constant, well timed messaging throughout a number of channels.

With 120+ ready-made attributes to section customers (together with traits, behaviors, preferences, and extra), Insider One empowered Vodafone’s advertising and marketing group to rapidly construct and launch new, expertly segmented campaigns to extremely focused audiences.

Learn the complete case research right here.

4. Prioritize safety and compliance at each step

In retail banking, your clients’ knowledge is their most beneficial asset and their deepest vulnerability.

Give it some thought: each transaction, each app login, each department go to generates a path of non-public info—from account balances to spending habits to residence addresses.

This knowledge is the lifeblood of personalization, enabling banks to supply smarter providers and extra related provides. However with nice knowledge comes nice accountability and important threat.

Knowledge breaches have turn into a relentless risk. Prospects know this, they usually’re holding banks accountable. They anticipate you to guard their knowledge as fiercely as they defend their very own wallets, they usually’re more and more keen to change banks in the event that they don’t really feel secure.

That’s why safety and compliance can’t be an afterthought; they must be woven into the very material of your omnichannel technique. Assembly rules like GDPR and CCPA is simply the beginning; it’s about constructing a tradition of information stewardship that earns belief and fosters loyalty.

The excellent news? You may make safety a aggressive benefit with Insider One. Right here’s how:

- Invisible safety: Create an omnichannel expertise that feels seamless, however operates on a basis of sturdy safety measures. This implies granular entry controls, real-time risk monitoring, and strict adherence to knowledge privateness rules.

- Empowered management: Give clients visibility into their knowledge and management over the way it’s used, to make them lively contributors of their safety.

Reshape the way forward for omnichannel banking with Insider One

Banks that cling to outdated programs threat turning into relics.

The excellent news? Assembly these expectations isn’t a pipe dream. It’s inside attain. With Insider One, you may rework disjointed interactions into seamless journeys.

Our AI-driven personalization, unified knowledge platform, and channel orchestration instruments aid you construct banking experiences which might be as fluid and intuitive as your clients anticipate.

Able to cease taking part in catch-up and begin main the pack? To be taught extra about Insider One, ebook a demo with our group or attempt the platform your self.