Assist CleanTechnica’s work by way of a Substack subscription or on Stripe.

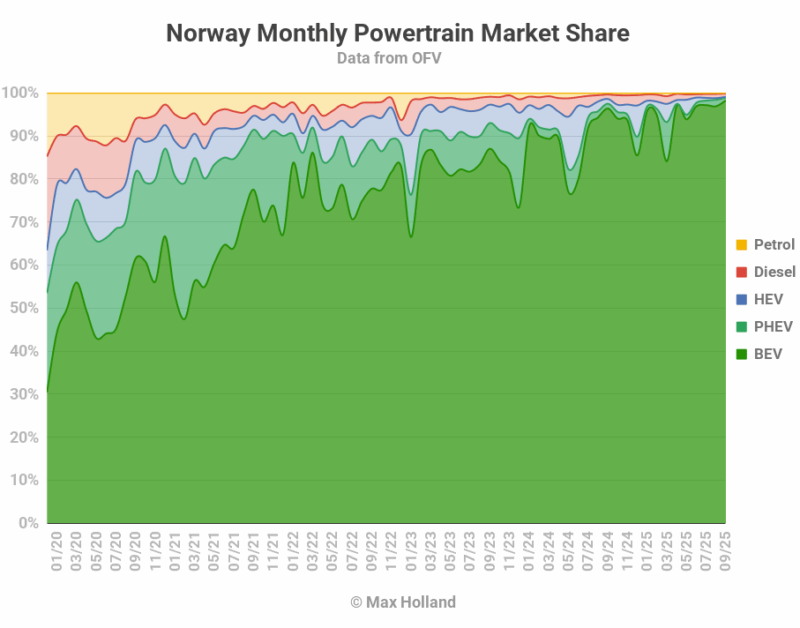

September noticed plugin EVs take a report 98.9% share in Norway, up from 97.5% yr on yr. BEVs alone took 98.3% share, additionally a report excessive. General auto quantity was 14,329 items, up some 11% YoY. The Tesla Mannequin Y was the best-selling automobile.

September’s auto market noticed mixed EVs take a report 98.9% share in Norway, comprising 98.3% full electrics (BEVs) and 0.6% plugin hybrids (PHEVs). These evaluate with YoY figures of 97.5% mixed, 96.4% BEV and 1.1% PHEV.

That is the fourth consecutive month of report mixed EV share, and the third consecutive month of report BEV share. This all means that the tax tweaks which got here in in the beginning of April have had their desired impact to additional disincentivize something aside from BEV purchases.

When it comes to the residual powertrains, PHEVs (0.6% share) are actually extra widespread than HEVs (0.2%), and petrol-only (0.2%), which appears rational. Sadly diesel-only powertrains (0.7%) are nonetheless sometimes forward of even PHEVs. This, nevertheless, seemingly solely displays that some area of interest segments nonetheless have few BEV or PHEV fashions on supply, mixed with the truth that diesels have a tried-and-tested picture of reliability for some consumers, which can be extremely valued in sure uncommon cases “simply in case”.

The existence of those hard-to-reach niches is frequent in expertise transitions the place marginal use-cases usually worth reliability, adaptedness, and predictability over the benefits of the newer expertise. Nonetheless, at solely 0.7% of the market (and regularly diminishing), diesel-only gross sales are usually not one thing to be overly involved about. For my part, diesel consumers shouldn’t be blanket-penalized (e.g. by ever increased taxes) with out understanding their wants and why EV choices are perceived as not but the fitting match for them (for infrastructure causes or in any other case). Within the fullness of time, additional advances in BEV (or PHEV) expertise, and much more ubiquitous and dependable charging infrastructure, will seemingly care for the wants and issues of those customers.

Finest-Promoting Fashions

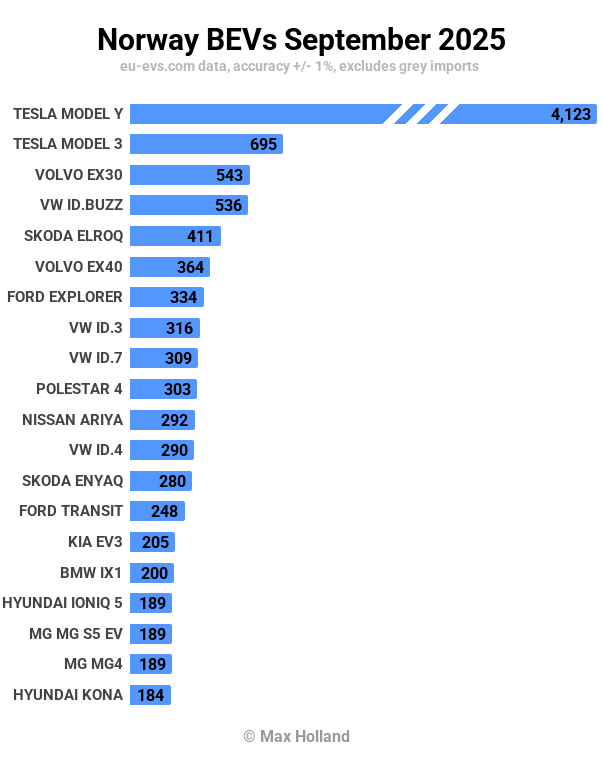

The Tesla Mannequin Y was as soon as once more the best-selling auto in Sweden, with an enormous 4,123 items offered in September. This represented round 29% of your complete auto market, and greater than the subsequent 10 fashions mixed.

Its sibling, the Tesla Mannequin 3 got here in second place, with 695 items. In third was the Volvo EX30, with 543 items.

Many of the high 20 faces are acquainted ones, with no outright newcomers becoming a member of the highest 20. Some regular month-to-month variations in rating occurred, particularly from these manufacturers that ship to this market in irregular quantity (e.g. Tesla, Polestar, Volvo, MG).

As for notable performances, the Skoda Elroq (which debuted in February) continued to steadily climb, reaching its highest rank of fifth in September, with a report quantity of 411 items. This can be a nice end result for Skoda.

The Ford Explorer noticed its highest quantity of the yr, with 334 items (and seventh spot). The Polestar 4 additionally noticed its highest ever quantity (303 items), and took a uncommon tenth spot. Nonetheless, as alluded to above, Polestar’s deliveries are extremely erratic (averaging 75 month-to-month items in July and August). We are able to chalk September’s elevated Polestar 4 numbers as much as a brief burst cargo to meet up with a requirement backlog, moderately than indicating a better degree of sustained demand.

There have been a few BEV debutants in September. MG Motor launched their new IM5 and IM6 fashions, with 20 and 24 items respectively. These are massive E-segment automobiles, with the IM5 being a sedan, and the IM6 an SUV. The IM5 begins from 399,000 NOK (€34,360) for the bottom 75 kWh battery (100 kWh non-obligatory), and the IM6 from 489,900 NOK (€42,200), coming as customary with the 100 kWh battery.

These new MGs come at reasonably priced costs for E-segment automobiles, particularly given the ~400 kW charging pace of the 100 kWh variants. For extra technical information on these new fashions, test the UK report from July, after they debuted over there. I can see the IM6 SUV doubtlessly doing properly in Norway, so let’s regulate them.

The opposite half-debut was for the upcoming Isuzu D-Max pickup truck, although simply registering a single unit for testing for now, because the D-Max can have its correct industrial launch in early 2026. We’ve coated the D-Max’s primary specs within the UK August report, so have a look over there for extra particulars.

Speaking of BEV pickup vehicles, the KGM Musso elevated from its August debut quantity of 5 items, as much as 29 items in September, a powerful begin for such a distinct segment automobile. The Maxus eTerron had seen showroom items in June, however first buyer deliveries in August (5 items), and elevated to fifteen items in September. Take a look again finally month’s report for a comparability between these two pickups. Briefly, the Musso is a barely extra modest pickup truck than the eTerron, however nonetheless provides loads of utility and vary for a lot of customers – and at a a lot cheaper price level (from 469,900 NOK, €39,900).

The brand new Mercedes CLA, which had debuted in August with 8 items, stepped as much as 27 items in September. Based mostly on its fast rise in neighbouring Sweden (already close to the highest 20 after simply 2 months on sale), the CLA might doubtlessly have loads additional to climb in Norway additionally.

August’s different newcomer, the Renault 4, elevated to twenty-eight items in September, and can climb increased from right here, doubtlessly near the highest 20 in some unspecified time in the future. Its sibling the Renault 5 is already seeing 100+ items per thirty days, and rating round thirtieth, with room to develop additional. The Renault 4 relies on the identical platform, however in a ten% bigger SUV form which is a greater match for Norwegian preferences. The Renault 4 would possibly thus be the higher vendor of the 2. Let’s regulate them.

As for different small-and-affordable BEVs, the Hyundai Inster took thirty third spot with 82 items. It’s too early to say whether or not its current month-to-month volumes of just below 100 items are a plateau, or only a pause on an extended ascent, so let’s regulate it. Because of some technical teething troubles (that are being resolved), the Citroen e-C3 is having a quieter time, with 54 items in September, down from its preliminary peaks (100+ items) within the spring. It nonetheless could get better. The BYD Dolphin Surf has nonetheless not launched in Norway, so there’s each prospect that the A & B segments will proceed to develop in quantity (and competitors) over the subsequent yr or so.

Let’s inspect the trailing quarter charts:

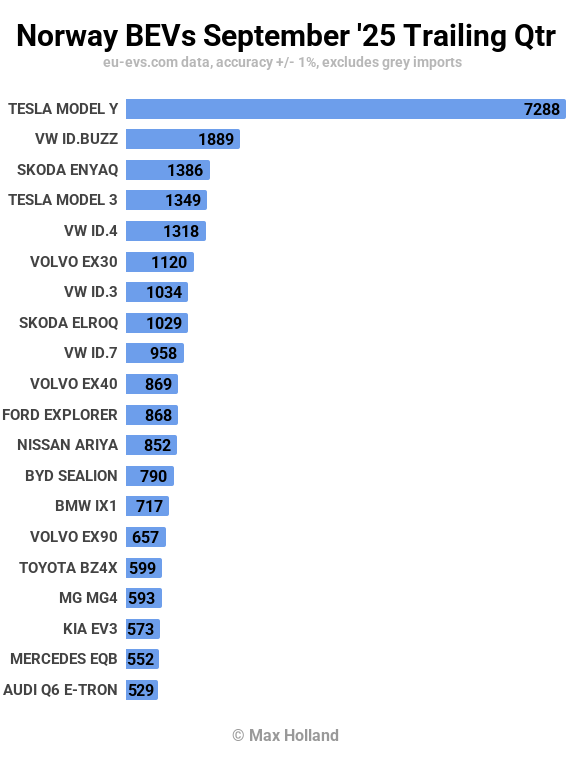

With an enormous August, and an even bigger September, the Tesla Mannequin Y has a monster lead, with extra quantity than the subsequent 5 fashions mixed. The Volkswagen ID. Buzz is in second, and the Skoda Enyaq is in third.

Essentially the most constant climber is the Skoda Elroq, now as much as eighth spot, from twenty first within the Q2 interval. It has additional to climb, and should attain the highest 5 by the tip of This autumn (relying on allocation).

Simply exterior the chart, in twenty second spot, the MG S5 is steadily bettering (from thirty third in Q2), and should but break into the highest 20 within the coming months.

We are able to additionally count on to see the Ford Explorer (now in eleventh) to doubtlessly climb additional within the close to time period, partially as a result of Ford usually has an finish of yr push to satisfy its fleet emissions necessities.

The very best ranked small-and-affordable BEV is the Renault 5, in thirty second spot, with 312 items in Q3 (up from 155 items in Q2). The Hyundai Inster is simply behind in thirty seventh, with 233 items (from 164 in Q2).

Fleet Transition Replace

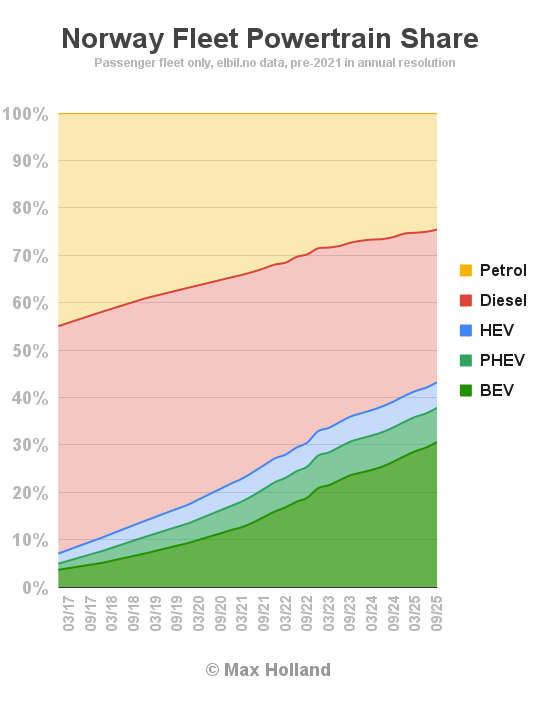

Up to date fleet information from the tip of Q3 exhibits a gradual enhance in EV share on the expense of each petrol and diesel powertrains. Mixed plugin share on the finish of Q3 stood at 37.8%, with 30.6% BEV. This is a rise over Q2’s share of 36.7% mixed, with 29.5% BEV.

We are able to see that BEV share has elevated by (a bit over) 1.1% over the three months. In the meantime, PHEV share is now simply previous its excessive level (round 7.2% of the fleet), as a result of PHEV gross sales peaked round 4 years in the past, and have now fallen to solely round 1% of the brand new automobile market. Their share of the fleet peaked round 18 months in the past, and can solely slowly diminish over the approaching years (by round 0.1% per yr within the close to time period), as a result of a lot of the PHEV fleet continues to be comparatively younger and never but close to retirement age.

Likewise the HEV fleet already peaked at round 5.4% share a few yr in the past, and new HEV additions (gross sales) have dropped off dramatically over the previous 18 months. Since this fleet is a bit older on common (with the Prius and related fashions having been offered for just a few a long time already), it can diminish at a barely increased charge than the PHEV fleet, seemingly by round 0.15% per yr within the close to time period.

The oldest automobiles within the fleet are diesels (on common) as these had their gross sales peak again within the 2008-2011 interval. They’re nonetheless the most important portion of the fleet, at 32.2%, however are at the moment dropping round 0.6% share each quarter (~2.5% per yr). Which means that the BEV fleet’s (rising) share will surpass the (shrinking) diesel fleet’s share earlier than the tip of this yr, as we are going to see within the end-of This autumn replace.

The petrol fleet is of “medium age”. As soon as diesels had handed their peak gross sales in 2011, petrols had been the perfect sellers till they had been overtaken by BEVs in 2018. This implies the typical petrol automobile is at the moment round 10 years previous and nonetheless has just a few years of service left. Petrols at the moment maintain 24.6% share of the fleet, and are at the moment dropping round 0.4% every quarter on common. The petrol fleet figures are sophisticated barely by seasonal deregistrations and re-registrations of older petrols that are used in the summertime months however hibernated throughout winter. General, petrols will seemingly fall below 20% of the fleet in round 3 years time.

Observe that fleet powertrain shares are just one part of what number of passenger KM get pushed yearly by every powertrain. New automobiles get pushed rather more (annual KM) than 10 yr previous automobiles, on common. The typical BEV is far newer than e.g. the typical diesel, and BEVs’ mixed annual KM have already overtaken that of diesels, though diesels are nonetheless barely extra quite a few inside the fleet.

To see these dynamic results, and the way they mix to affect the diminishing demand for street fuels, see my deep dive report on fleet dynamics.

Outlook

Norway continues to make constant and rational progress within the EV transition, with constant coverage assist and shopper acceptance of the brand new expertise. Solely China comes near the rational transition that Norway has pioneered (arguably extra spectacular as a result of China shouldn’t be almost as rich as Norway, and has to really construct these automobiles at immense scale, the place Norway can merely purchase them from exterior, in comparatively negligible volumes). Sweden, France, Germany, the US, and plenty of different areas, have been erratic, inconsistent, and albeit usually insincere in making the transition.

Norway’s auto market has grown 23.5% yr to this point, a very good signal, since that development (now successfully all BEVs) is dashing the fleet transition.

As a reminder, Norway’s macroeconomic figures are usually extremely erratic as a result of massive dimension of public spending, and the disproportionate affect that fossil-fuel gross sales (and their variable pricing) have on nationwide accounts. The most recent YoY GDP figures stay these from Q2 2025, with an enormous swing to detrimental 2.1%. Inflation crept as much as 3.5% in August (newest information) from 3.3% in July, and rates of interest diminished additional, to 4% (from 4.25%) in mid-September. Manufacturing PMI elevated modestly to 49.9 factors in September, from 49.6 factors in August.

What are your ideas on Norway’s auto market, and what can the remainder of the world be taught from Norway’s strategy to the transition? Or maybe not be capable of simply replicate? Please bounce into the feedback beneath to share your views.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our day by day e-newsletter, and observe us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our day by day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if day by day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage