The provision of latest properties listed on the market within the UK has now surpassed 1.5 million yr so far, whereas gross sales agreed (SSTCs) exceed 1 million, in response to information from TwentyEA.

All eyes within the property sector at the moment are on the Funds on 26 November, with brokers eager to see how upcoming insurance policies may have an effect on housing provide and purchaser demand.

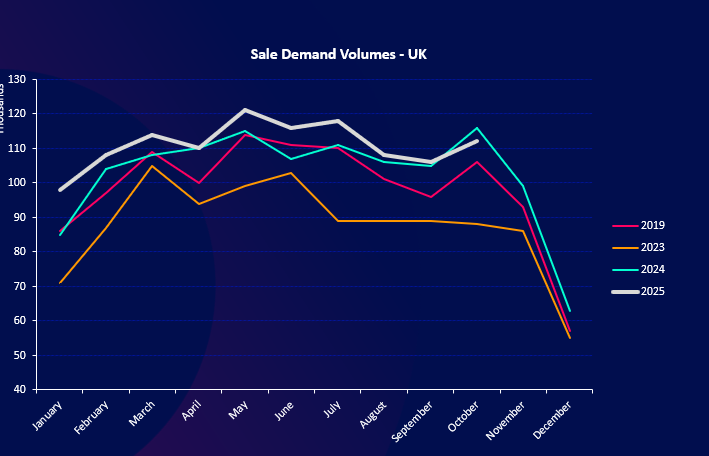

For now, each provide and demand stay resilient, up 3.3% and 4.1% respectively in contrast with final yr. Purchaser demand is at its highest stage since 2022, with a present demand-to-supply ratio of 72.4%, exceeding figures for each 2023 and 2024.

Though demand fell by 2.7% year-on-year in October, that is more likely to characterize solely a brief blip. October 2024 noticed exceptionally excessive exercise as falling rates of interest prompted consumers to hurry transactions forward of the 30 October Funds.

Property varieties

Whereas each demand and provide have risen for all property varieties, there are nonetheless adjustments occurring with indifferent and semi-detached homes getting extra fashionable. For indifferent properties, the demand to produce ratio has risen by 4.6% versus the prior yr.

Costs

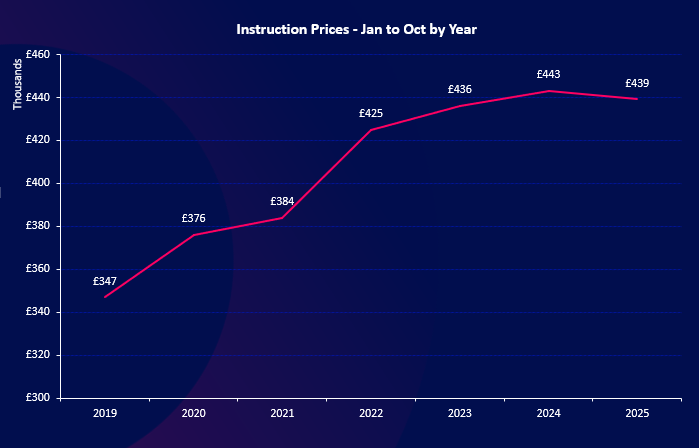

The typical authentic instruction value in 2025 has fallen by 0.8% (£3,700) within the final yr and on a regional foundation, instruction costs are principally growing within the North and Midlands, while costs within the south are static or falling.

Inside London is the one area to see yr on yr costs fall by greater than 3%.

In the meantime, the variety of value reductions have now exceeded a million thus far this yr and is 14% greater YoY.

The share of properties having value reductions has additionally elevated, however solely marginally. In 2025 thus far, 38.7% of concluded listings had a minimum of one value discount, in 2024, this was 38.0%.

In contrast with final yr, the worth adjustments have elevated in all bands with £1m+ properties standing out, the place discount charges have elevated by 3 proportion factors.

Basically, value reductions are decreasing within the North and growing in London and the South. Inside London has seen a 2.9 proportion level enhance and that is by far the worst affected area of the UK.

Katy Billany, govt director of TwentyEA, mentioned: “The info reveals that each provide and demand stay resilient regardless of a dip in October and hopefully we’ll begin to see demand growing once more as soon as now we have some readability following the Autumn Funds.

“With extra properties in the marketplace, motivated sellers are adjusting their expectations and providing extra aggressive pricing, resulting in elevated ranges of value reductions, now a couple of million thus far this yr.

“At this level, all eyes are focussed on the Chancellor’s Funds, which clearly falls a lot later than regular, to see what coverage adjustments could emerge. Any measures that enhance affordability or encourage transactions will assist maintain the optimistic momentum we’ve seen throughout most areas all through 2025.”