Assist CleanTechnica’s work via a Substack subscription or on Stripe.

The story of america corn ethanol business is a narrative a few sector that grew quickly below a really particular set of coverage, expertise and market circumstances. It crammed a spot when gasoline demand was rising, when local weather coverage targeted on incremental change, and when EVs have been nonetheless a distinct segment. It turned a serious a part of the Midwestern political economic system. It formed land use patterns. It supported hundreds of farmers and dozens of rural communities constructed round regular demand for transport gas. That world is shifting and the indicators level towards a twenty 12 months horizon that appears very totally different from the earlier twenty, with very important implications for the Midwest’s economies and certain politics.

Corn ethanol grew from a small program targeted on oxygenates right into a nationwide business producing over 16 billion gallons yearly, about 48 million metric tons. The Renewable Gasoline Commonplace created assured demand by requiring refiners to mix growing quantities of ethanol into gasoline. Direct subsidies via the Volumetric Ethanol Excise Tax Credit score helped broaden capability. By the late 2000s the business had grow to be giant sufficient to carry political weight in Iowa, Illinois, Minnesota and Nebraska. Ethanol vegetation turned anchor employers. Farmers gained a brand new purchaser that consumed almost 40% of the nationwide corn crop. The system turned predictable and self reinforcing. All gasoline offered within the nation now has about 10% ethanol added, with some increased blends accessible in some locations. As soon as direct subsidies expired, the mandate and a big fleet of inside combustion automobiles stored the business steady. That stability is now being examined by structural adjustments in transportation and power.

The primary problem seems within the gasoline market itself. EIA information from 2015 via 2019 reveals completed motor gasoline stabilizing at roughly 140 billion gallons a 12 months. The publish pandemic rebound by no means reached that vary once more. By 2024 gasoline demand had slipped under pre pandemic ranges though the inhabitants was bigger than in 2019. The shift is just not a statistical quirk. Effectivity positive aspects, hybrid penetration and improved powertrain design are pushing gasoline demand down. Even modest EV adoption impacts gas consumption greater than most individuals count on as a result of every EV replaces a whole family’s gasoline demand, not a small slice of it. Hybrid and earn a living from home fashions which can be frequent after COVID additionally inhibit demand. Gasoline peaks are not often jagged occasions. They plateau after which start sluggish however sturdy declines. Ethanol demand sits inside that shrinking pool. Rising mix charges can not compensate if the bottom declines 12 months after 12 months.

E15, a mix of 15% ethanol and 85% gasoline, creates a small carry for producers, however there is no such thing as a critical nationwide transfer towards E30 or increased mid degree blends. The political power behind E15 has come from arguments about provide enlargement and client value, not carbon depth or long run technique. E30 requires totally different infrastructure and testing. It requires automakers to warrant engines for increased blends. It requires retail investments that stations are reluctant to make with out ensures. None of that’s materializing. States like California and New York now allow E15, however these choices have been framed as value and provide flexibilities reasonably than a brand new power path. Ethanol sits in these states as an accepted a part of the gasoline period, not a central ingredient of long run local weather coverage. In markets that matter most for future tendencies the path is evident. The strategic focus is electrification.

California and New York are sometimes handled as outliers in nationwide conversations. They aren’t outliers. They’re lead indicators in car transition. California’s superior clear vehicles coverage will push new automotive gross sales towards 100% zero emission by 2035. New York has adopted the identical path. These are prosperous states with giant populations and plenty of vehicles. Larger ethanol blends in these states quantity to small changes on the margins of a system that’s already pivoting towards EVs. As EV shares rise in coastal states, gasoline consumption falls in absolute phrases. Even when some drivers maintain on to older automobiles for longer, the burden of latest gross sales adjustments the slope of long run demand. These states signify sufficient automobiles that their selections affect nationwide averages. Ethanol suits into their close to time period gas combine, however it isn’t shaping their long run path.

Export markets, one thing that grew lately, see comparable headwinds. Previously few years US ethanol exporters have loved sturdy demand from Canada, the UK and components of Southeast Asia. These markets are shifting. Canada is tightening its clear gas rules and growing its EV penetration. The UK and EU have sustainability standards that restrict long run enlargement of meals primarily based biofuels. India is constructing a home ethanol business utilizing sugarcane and grain feedstocks. Brazil is increasing corn ethanol capability of its personal. OECD and FAO analyses challenge that almost all future world ethanol development will probably be met domestically reasonably than via imports. In addition they challenge that whole world ethanol commerce will stay solely a small fraction of manufacturing. Export contraction is extra doubtless than export development, and the remainder of the world is transferring sooner to EVs and now, with Trump’s tariffs, transferring away from dependency on US imports.

The ethanol to jet pathway seemed to be probably the most promising new outlet, nevertheless it relies upon closely on regulatory certainty. Alcohol to jet gas can meet ASTM requirements and mix seamlessly with petroleum jet. Airways are occupied with any provide that may assist them meet long run local weather pledges. The economics are fragile. Manufacturing prices stay increased than petroleum jet. Carbon depth scoring determines eligibility for tax credit, and it requires each farming adjustments and seize and sequestration of CO2 from fermenters to realize sufficiently low depth. These credit require steady coverage. The removing of the sustainable aviation gas bonus credit score on the finish of 2025 below Trump omnibus invoice shifted the economics considerably. The discount from a possible $1.75 a gallon credit score to a $1.00 credit score lower the margin for many proposed tasks. Builders now face a shorter coverage horizon, extra uncertainty and capital markets which can be more and more delicate to coverage volatility. Some excessive profile tasks have already stalled or been rescoped. Ethanol to jet stays a doable development space however it isn’t a agency basis for your entire business.

In different work on aviation I’ve projected that world passenger and cargo demand won’t hold rising on historic 4% annual curves, however will flatten as China’s development slows, distant work persists and inhabitants peaks. In that state of affairs fossil kerosene peaks round 2030 under 2019 ranges after which declines over the remainder of the century as batteries and biofuels take over a lot of the power demand for flights. Electrical flight will probably be cheaper, 1,000 km hybrid electrical turboprop ranges totally on batteries viable, whereas worldwide flights with sustainable aviation fuels will probably be costlier. Whereas the USA has the very best passenger kilometers per resident the world by a hefty margin, 60% to 70% are within the vary to be electrified, and ticket value differential will favor these flights with extra visitors. Globally, excessive pace rail is eradicating passengers from airplane seats, and world inhabitants development is already slowing, with the flight heavy west seeing growing old demographics.

All of those components will cut back the demand for liquid fuels for aviation. Biokerosenes together with ethanol to jet bridge the remaining lengthy haul missions throughout current airframes. The result’s a protracted tail of liquid gas use concentrated nearly completely in intercontinental aviation by 2100, with quick haul and regional providers totally electrified and plenty of small airports revived as electrical regional mobility hubs.

I’ve additionally argued that private transportation in america is uniquely laborious to decarbonize in comparison with Europe or China due to structural selections made after World Struggle II. Low-cost oil, racialized planning and deliberate dispersion insurance policies pushed folks into very low density suburbs and weakened passenger rail so completely that Individuals now depend on very giant vehicles and frequent home flights for fundamental mobility. Automobiles and light-weight vehicles account for effectively over half of US transport emissions and highway automobiles of all sizes contribute greater than 80% of the sector whole, but the nation nonetheless lags friends on EV adoption and transit funding.

That mixture of maximum sprawl, giant automobiles, weak rail and entrenched freeway infrastructure means america has to push tougher on each electrification and concrete type simply to get to the beginning line that different wealthy nations are already standing on. It additionally signifies that in america, liquid fuels for vehicles and aviation keep within the image longer than they’d in a denser, rail oriented system, which is another reason to count on corn ethanol and different biofuels to face a protracted, messy transition as an alternative of a clear break. Nevertheless it doesn’t imply that electrification received’t eat inside combustion gas demand for lunch, it simply means it will likely be a extra leisurely meal.

Marine fuels are typically offered as a serious alternative, however right here too the outlook is just not for development and ethanol is just not the molecule of alternative. Beginning with demand, 40% of all delivery tonnage is of fossil fuels, and that’s in structural decline. One other 15% is uncooked iron ore, often steaming to the identical ports coal is headed to. That too is in structural decline with renewable electrical energy primarily based derusting of iron ore to make iron rather more viable nearer to coal mines, growing the worth whereas lowering the tonnage of exports. World metal demand can be in decline, as China has completed the huge infrastructure growth and is getting into a decrease upkeep cycle because the developed world did within the second half of the twentieth Century. Different nations have entry to low-cost software program and mass timber that considerably reduces metal demand in new buildings, and aren’t going to be constructing the huge components, heavy business and ports that China did. Structurally, 55% of whole delivery tonnage is in decline.

Additional, electrification is coming for delivery as effectively. 700 unit container ships with swappable containerized batteries are servicing 1,000 km routes on the Yangtze in China. 2,100 passenger totally electrical ferries are on order and being examined within the water already. Hybridization of ocean going ships is nearly inevitable because the economics of grime low-cost batteries, clear and cheap electrons, and rather more pricey biofuels radically alter present assumptions. The mixture ends in a lot much less delivery gas sooner or later than as we speak. It’s not a development market wanting in desperation for ethanol.

US corn ethanol rhetoric factors to giant delivery firms experimenting with multi gas blends that embrace ethanol. The worldwide delivery sector will use monumental quantities of gas even with declines and small mix shares indicate giant potential ethanol volumes. The caveat is that delivery is already transferring towards biomethanol and electrification. These power carriers provide higher power density or easier dealing with and are aligned with long run zero carbon methods. Trials that embrace ethanol are exploratory. There isn’t a regulatory anchor for ethanol in delivery akin to the mandates in highway transport within the early 2000s. There may be additionally a aggressive drawback. Sugarcane ethanol from extra tropical areas has a decrease carbon depth than US corn ethanol and suits extra comfortably inside worldwide carbon accounting. Marine fuels may soak up some gallons, however they don’t plausibly soak up the multi billion gallon hole created by declining highway gas use.

Chemical feedstocks are an actual however restricted alternative. Ethanol can function a platform for ethylene, acetic acid and different industrial chemical substances. Some firms in Brazil already function this fashion at industrial scale. These markets worth carbon depth, traceability and steady provide. They don’t require the volumes that highway transport does. Even optimistic eventualities for ethanol primarily based chemical substances solely soak up one or two billion gallons. The hole between that determine and present gas use is just too giant to bridge.

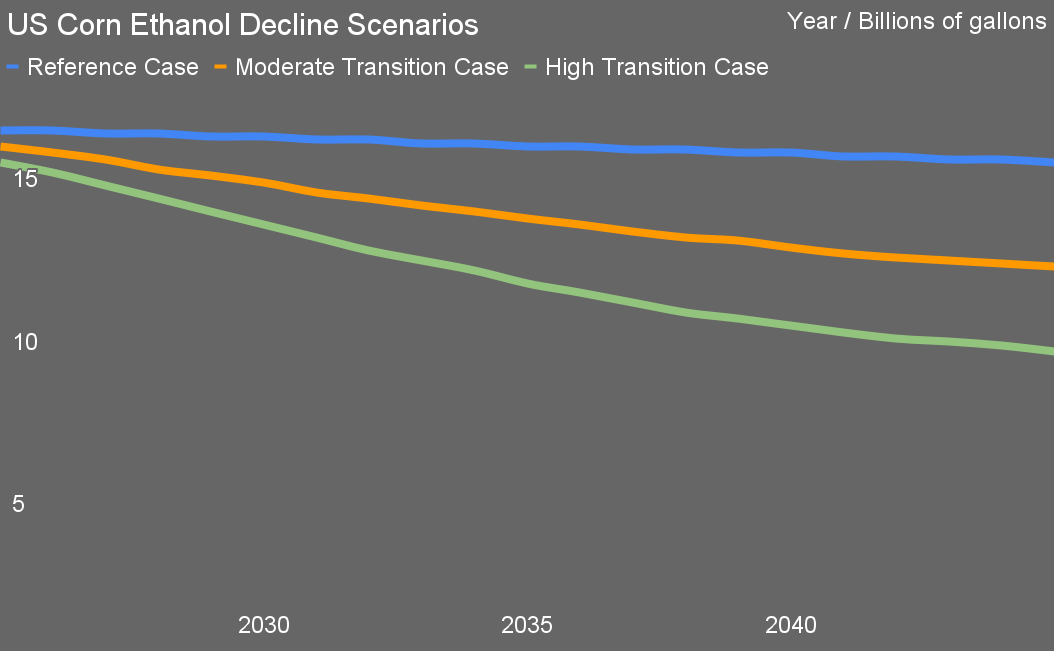

A helpful approach to consider the following twenty years is thru state of affairs evaluation. In a reference case primarily based on present federal coverage and modest EV adoption, ethanol manufacturing holds roughly flat. Mix charges climb barely. Exports stay regular. SAF provides a small quantity of additional demand. The business seems lots like as we speak with barely extra stress on the margins. In a reasonable case, EV adoption accelerates in step with world patterns. Gasoline demand falls 30% to 40%. Mix charges rise towards E15 however go no additional. Exports plateau. SAF struggles with coverage instability. Ethanol manufacturing falls 20% to 35%. In a excessive transition case, EVs scale rapidly throughout america, coastal states speed up their mandates and world automotive provide chains ship decrease value EVs sooner than anticipated. Export markets construct home manufacturing. SAF coverage stays unstable. Ethanol manufacturing falls on the order of 40% to 50%. None of those numbers are exact forecasts, however they describe affordable envelopes for planning.

The regional financial results of even a reasonable contraction will probably be important. Ethanol vegetation anchor many rural communities. They type a part of the idea that helps grain handlers, trucking companies and tools sellers. A discount in ethanol demand reduces native corn costs and impacts land values. Farmers will shift into different crops or modify rotations however that takes time. Some ethanol vegetation will diversify into increased worth co merchandise like protein concentrates or biochemicals. Others will shut or consolidate. The transition won’t be even throughout the Midwest. Crops with entry to low carbon electrical energy, carbon seize pathways or diversified product streams will adapt extra readily. Crops with excessive working prices or restricted entry to low carbon inputs will wrestle.

A lot of the communities constructed round corn-ethanol vegetation should not prosperous as we speak. They’re typically steady, middle-income rural cities whose economies rely upon agriculture, just a few industrial anchors and a small service base. Ethanol vegetation increase native incomes relative to purely farming counties as a result of they add processing jobs, assist a community of trucking, upkeep and engineering companies and strengthen corn costs inside a 30 to 60 mile radius. That impact improves family earnings and native tax income, nevertheless it doesn’t flip these areas into high-income areas. Lots of the counties with the heaviest ethanol focus nonetheless have below-average median family incomes in comparison with nationwide figures, decrease inhabitants development and restricted financial diversification. Ethanol vegetation present stability reasonably than affluence, which is why the prospect of long-term demand decline issues a lot. If the first industrial purchaser in an already skinny native economic system begins to shrink, the communities round it have little buffer and fewer various employers to soak up the shift. The mixture has the potential to imply an additional rural hollowing out and depopulation.

There’s a credible, long-run chance that declining corn ethanol demand might open the door to giant scale rewilding in components of the Midwest, however it might happen inconsistently with out sturdy federal and state steerage, and solely below sure financial circumstances. A big share of the land used for steady corn as we speak is just not prime cropland. A lot of it sits on marginal soils, areas liable to erosion, floodplains, former prairie that was introduced below cultivation in the course of the ethanol growth, or areas the place profitability will depend on excessive fertilizer inputs and regular native consumers. When an ethanol plant closes or reduces consumption by half, the weakest floor turns into laborious to justify financially. Farmers confronted with decrease native corn costs, increased transport prices to succeed in distant markets, and decrease returns per acre usually transition marginal parcels first. That transition can take the type of diminished tillage, grassland restoration, enrollment in conservation applications or leasing land to wildlife businesses or personal conservation teams. Federal conservation applications have already got ready lists in lots of states, and a sustained decline in corn demand would enhance curiosity in enrolling acres that not generate dependable income.

Rewilding doesn’t imply a full return to tallgrass prairie throughout total counties. It often begins with patches of land taken out of annual row cropping and transformed to blended grasses, wetlands or riparian buffers. Over time, these areas present habitat, enhance water high quality and cut back nutrient runoff. In areas with persistent flood dangers or groundwater stress, reverting parts of corn acreage to pure cowl can even ease public infrastructure prices. Some landowners will see worth in carbon markets if these markets grow to be extra credible. Others will companion with conservation organizations that mix ecological restoration with leisure or grazing leases. There’ll nonetheless be sturdy agricultural manufacturing on the very best land, however the general mosaic shifts. A sustained 40% to 50% decline in ethanol demand over twenty years would regularly launch hundreds of thousands of acres from strict commodity manufacturing stress, and a portion of these acres would movement into rewilding as a result of it turns into probably the most rational financial alternative for land that can’t compete effectively in a publish ethanol panorama.

There are viable paths ahead for a lot of producers. Some will spend money on carbon seize to decrease their gas’s measured carbon depth. Some will pursue biorefinery methods that deal with ethanol as one output in a broader product combine. Others will discover partnerships in chemical substances, specialty proteins or inexperienced ammonia. The business that emerges will probably be leaner and extra various than the one which grew below the Renewable Gasoline Commonplace. The talent units, infrastructure and expertise inside these firms are invaluable in new power and supplies markets. The query is how briskly they will pivot.

The massive scale circumstances that supported corn ethanol for twenty years are altering. The worldwide automotive business is electrifying. Regulatory frameworks in main importing nations are turning towards zero emission automobiles and low carbon fuels with strict sustainability standards. Home gasoline demand is softening in methods that can proceed and certain speed up. The coverage basis for ethanol to jet stays unstable. These components add as much as a long run surroundings the place a contraction of the US corn ethanol sector is extra believable than continued development. A decline of 20% to 50% is an inexpensive planning vary relying on how rapidly EVs scale and the way efficiently producers diversify. The subsequent twenty years will take a look at the business’s potential to adapt to a world the place highway fuels are not the first engine of power demand.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our day by day e-newsletter, and observe us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our day by day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if day by day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage

, GeeFi (GEE) or Cardano (ADA)? Why Analysts Say the Newcomer Ought to Get Extra Consideration This Winter")

![Why trendy dentists should prepare like pilots [PODCAST]](https://i0.wp.com/kevinmd.com/wp-content/uploads/Design-3-scaled.jpg?w=330&resize=330,220&ssl=1 "Why trendy dentists should prepare like pilots [PODCAST]")