Welcome to the fortieth UK property market stats present of 2025, your weekly TV programme on the UK housing market.

This week, I’m joined by Iain White, ex-Romans boss and property Company coach and thought chief, as we unpack the important thing headlines from the week ending Sunday twelfth October 2025.

🔍 Key Market Headlines – Week 40, 2025

✅ New Listings

- 32.7k new properties got here to market this week, down as anticipated from 34.3k final week.

- 2025 weekly common: 36.1k.

- 9 yr week 40 common :33.4k

- Yr-to-date (YTD): 1.44m new listings, 2.2% increased than 2024 YTD (1.41m) and 10% above the 2017–19 common (1.31m).

✅ Worth Reductions

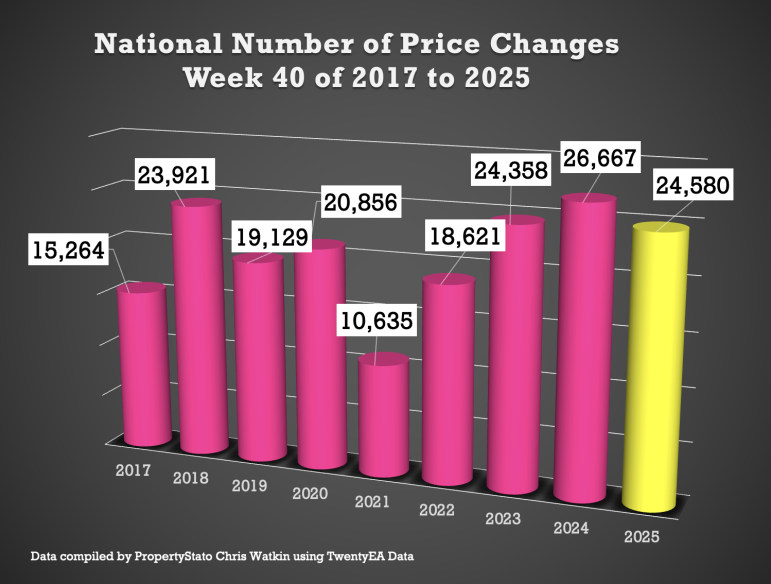

- 24.6k reductions this week, barely increased to final week at 25.6k.

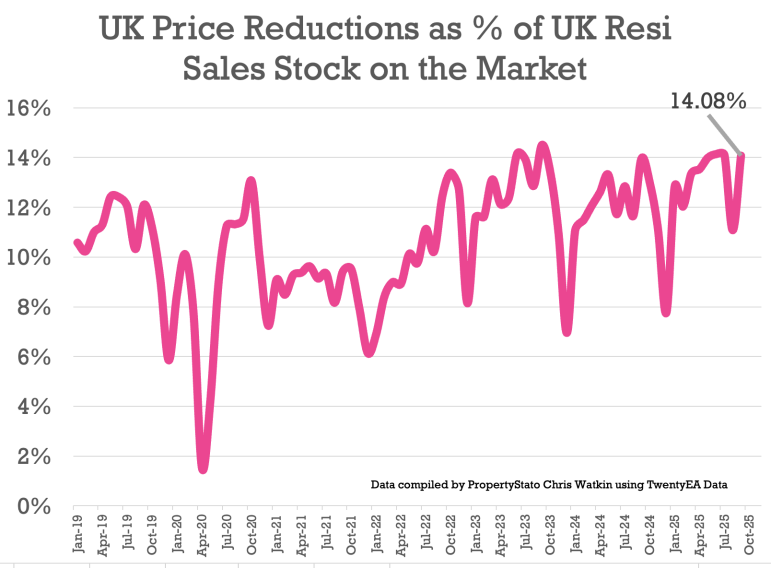

- Enhance within the variety of properties in the marketplace being diminished in September to 14.1%. In August, it was 11.1% (everybody should have been on vacation!), while it was 14.1% in July and 14% in June.

- 2025 common thus far: 13.2%, versus the five-year long-term common of 10.74%.

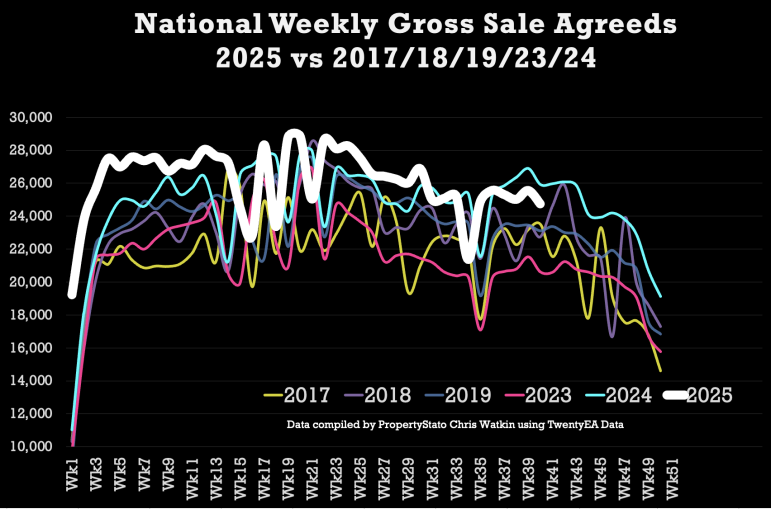

✅ Gross sales Agreed

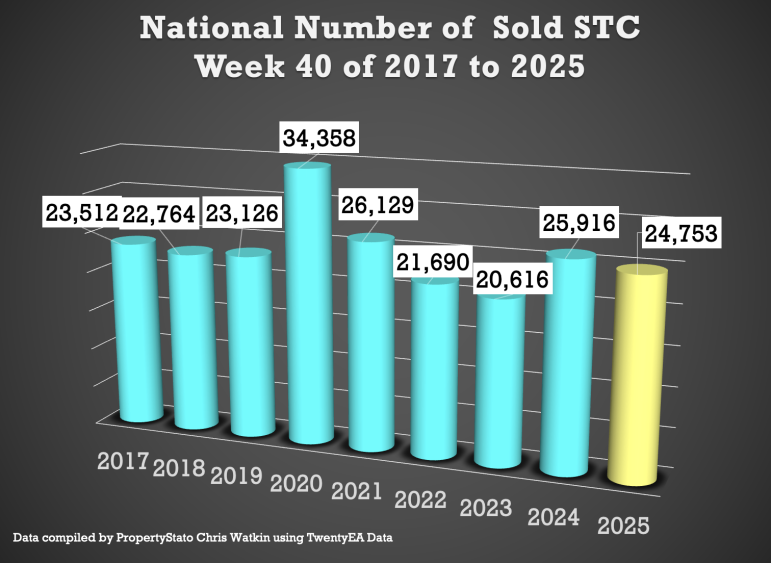

- 24.8k properties offered topic to contract this week, down as anticipated from 25.6k final week.

- Week 40 common (for final 9 years) :24.8k

- 2025 weekly common : 26.1k.

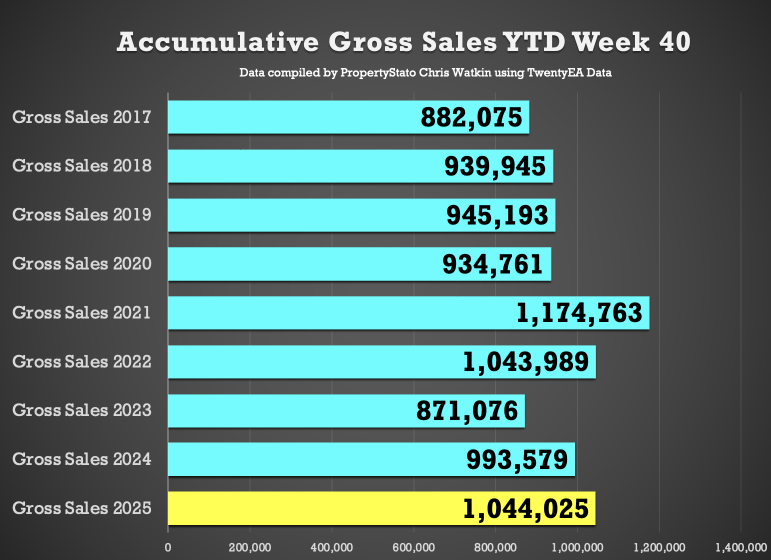

- YTD: 1.044m product sales, which is 5.1% forward of 2024 (994k) and 13.2% above the 2017–19 common (922k).

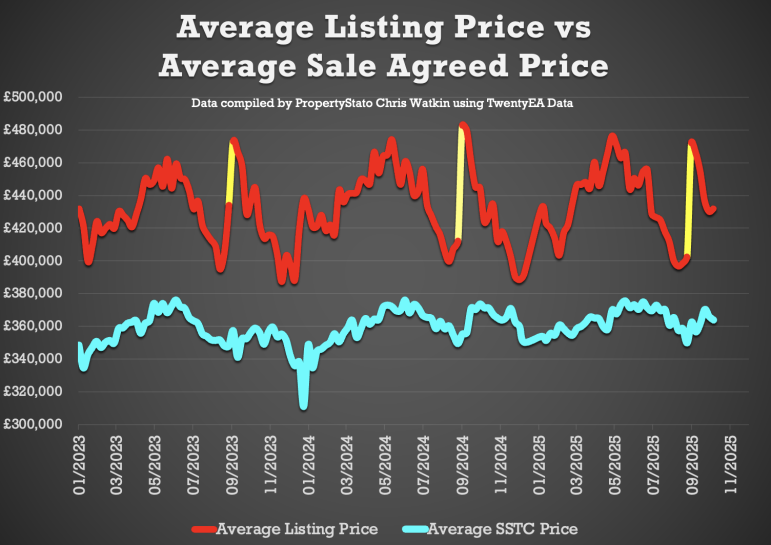

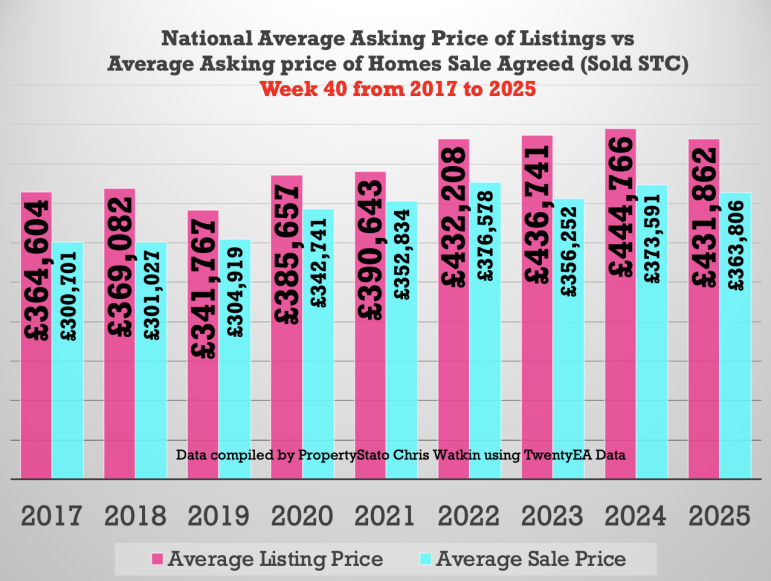

✅ Worth Diff between Listings & Gross sales

- Common Asking Worth of listings final week £432k vs Common asking worth of Gross sales Agreed (SSTC) – £364k

- 18.7% distinction (long run 9 yr common is 16% to 17%).

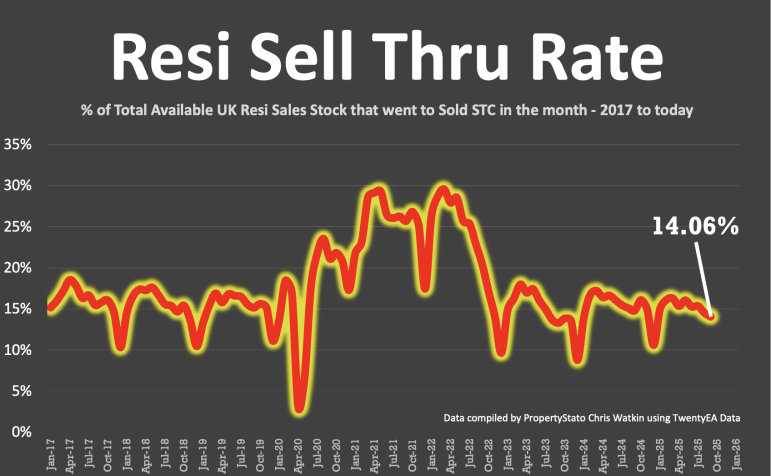

✅ Promote-By Charge

- 14.1% of properties on brokers’ books went SSTC in September.

- Down from 14.5% in Aug, 15.4% in July, 15.3% in June, and 16.1% in Could.

- Pre-Covid common: 15.5%.

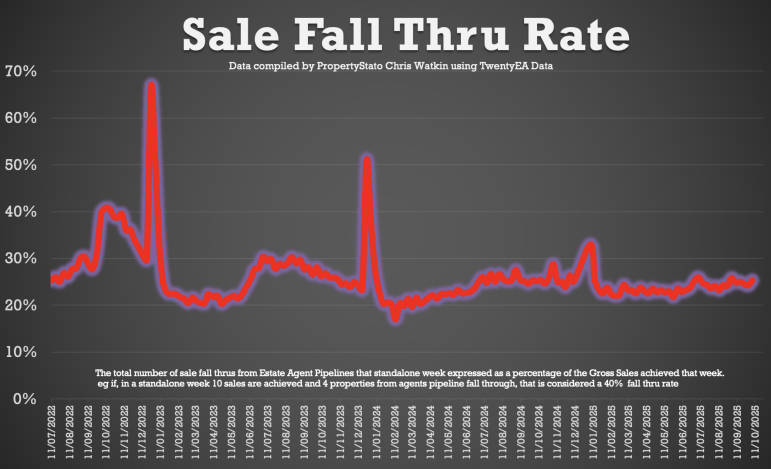

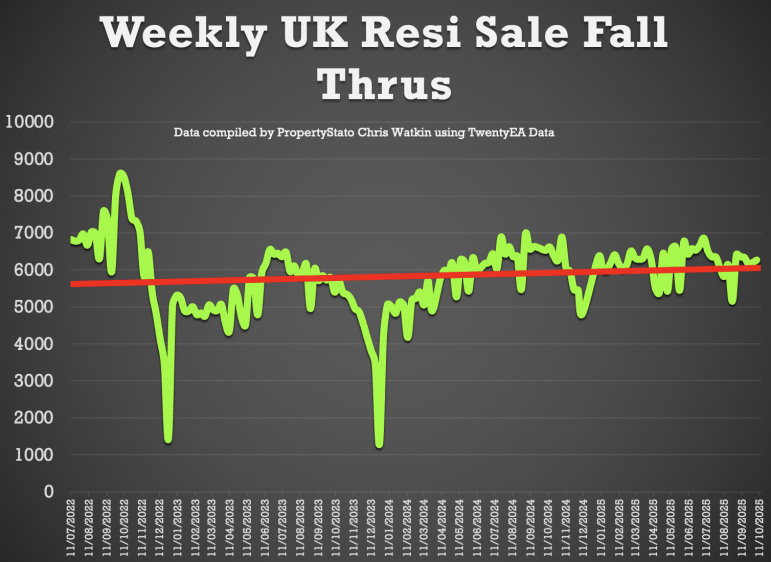

✅ Fall-Throughs

- 6,262 fall-throughs final week (pipeline of 510k residence Offered STC).

- Weekly common for 2025: 6,562.

- Fall-through charge: 25.3%, up from 24.6% final week.

- Lengthy-term common: 24.2% (post-Truss chaos noticed ranges exceed 40%).

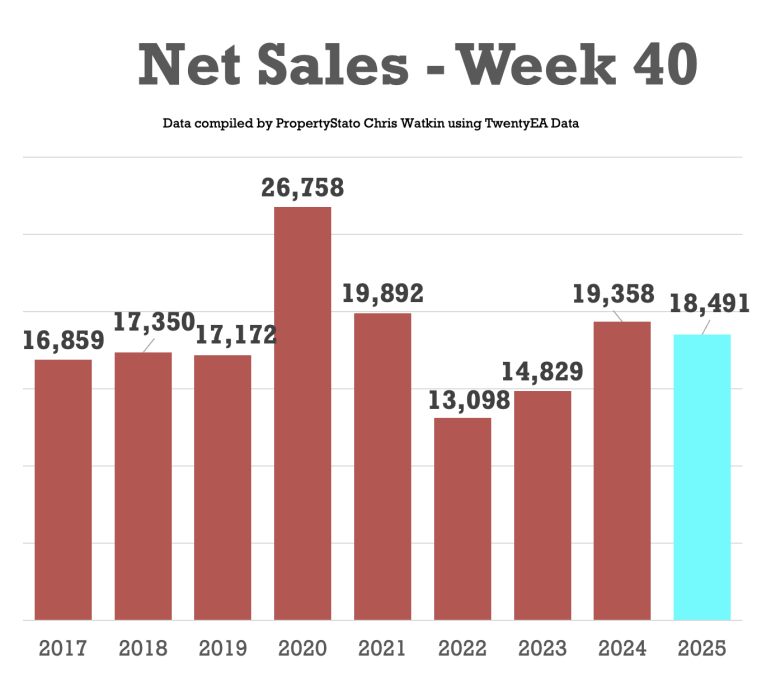

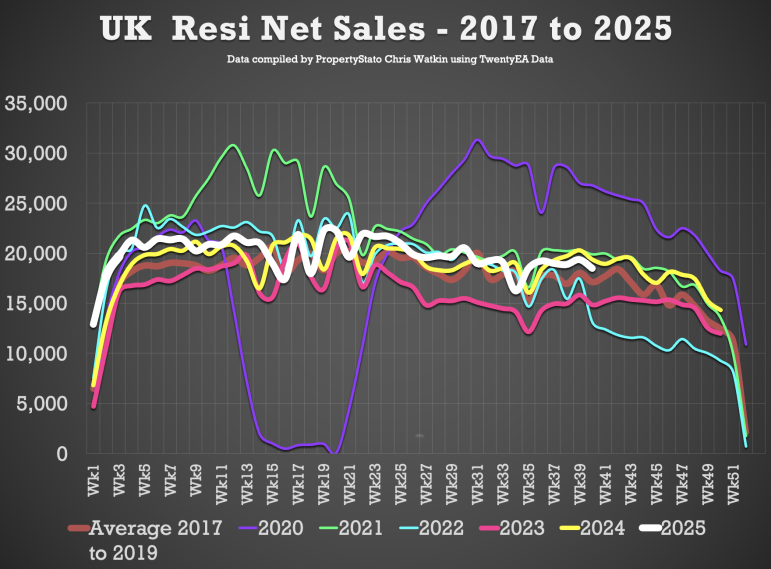

✅ Internet Gross sales

- 18.5k internet gross sales this week, up from 19.4k final week.

- 9-year Week 40 common: 18.2k.

- Weekly common for 2025: 19.9k.

- YTD: 795k, which is 4.3% forward of 2024 (762k) and 10% above 2017–19 (724k).

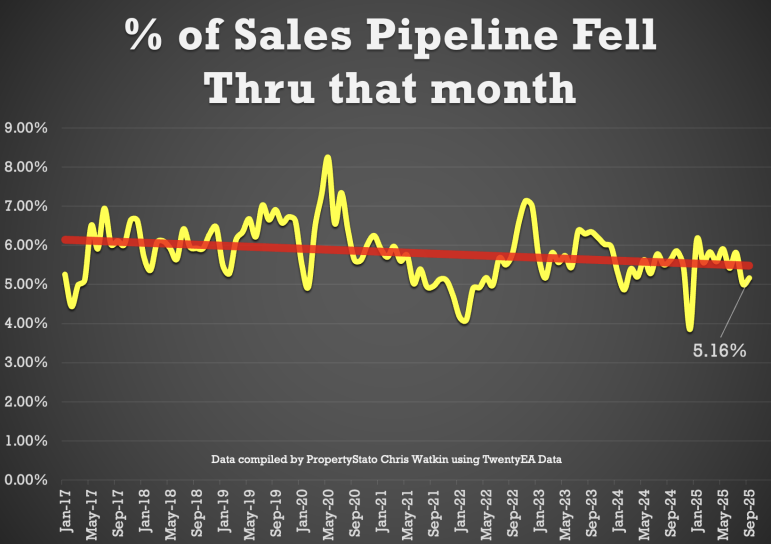

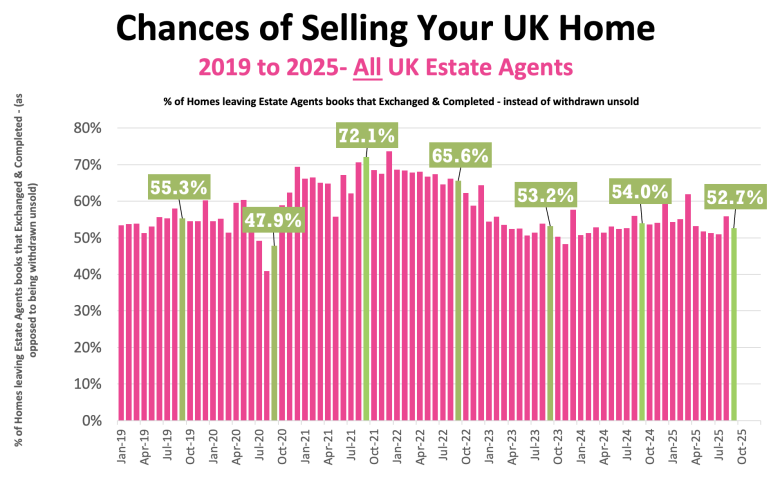

✅ Chance of Promoting (% that Alternate vs withdrawal)

- Preliminary September Stats : 52.7% of properties that left brokers’ books exchanged & accomplished. (Observe this can change as extra September stats are available in all through October)

- August :55.8% / July: 50.9% / June: 51.3% / Could: 51.7% / April: 53.2%.

✅ Inventory Ranges

- 751k properties in the marketplace at first of October, 4% increased than October 2024. (723k)

- 510k properties in gross sales pipeline on the first October, 2% increased than 12 months in the past.

✅ Home Costs (£/sq.ft)

- October 2025 agreed gross sales averaged £336.54 per sq.ft.

✅ Leases

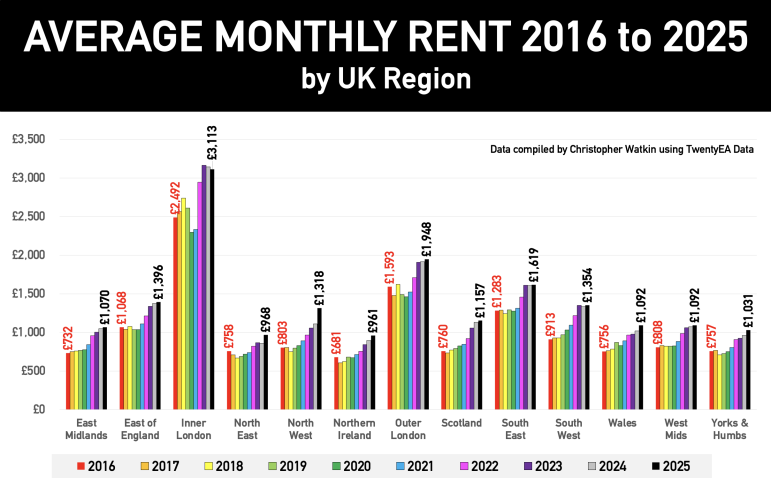

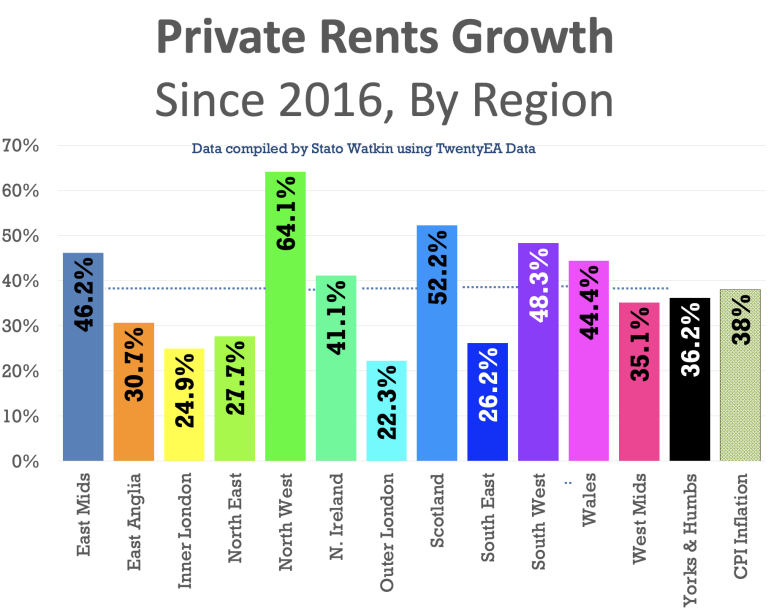

- Common Month-to-month Rents by area

· East Midlands – £1,070 (Development since 2016) – 46.2%

· East Anglia – £1,396 (Development since 2016) – 30.7%

· Inside London – £3,113 (Development since 2016) – 24.9%

· North East – £968 (Development since 2016) – 27.7%

· North West – £1,318 (Development since 2016) – 64.1%

· Northern Eire – £961 (Development since 2016) – 41.1%

· Outer London – £1,948 (Development since 2016) – 22.3%

· Scotland – £1,157 (Development since 2016) – 52.2%

· South East – £1,619 (Development since 2016) – 26.2%

· South West – £1,354 (Development since 2016) – 48.3%

· Wales – £1,092 (Development since 2016) – 44.4%

· West Mids – £1,092 (Development since 2016) – 35.1%

· Yorks & Humberside – £1,031 (Development since 2016) – 36.2%

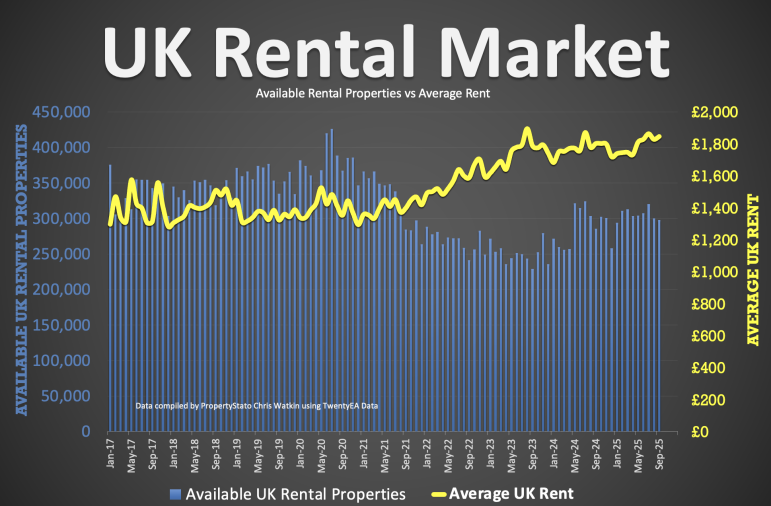

- Common UK hire in September – £1,846 – a progress 2.44% from Sept 2024

- 297k rental properties had been accessible in Sept ’25 (286k – Sept 24 & 229k in Sept ’23).

✅ Native Give attention to the Present:

Redhill & Reigate

Every day information electronic mail from EYE

Enter your electronic mail beneath to obtain the newest information every morning direct to your inbox.