This week’s UK Property Market Stats Present for the week ending Sunday thirtieth November 2025 (week 47) options Steph Vass from TAUK. Collectively, we evaluation the important thing information and developments from the week’s exercise within the property market.

✅ General Image

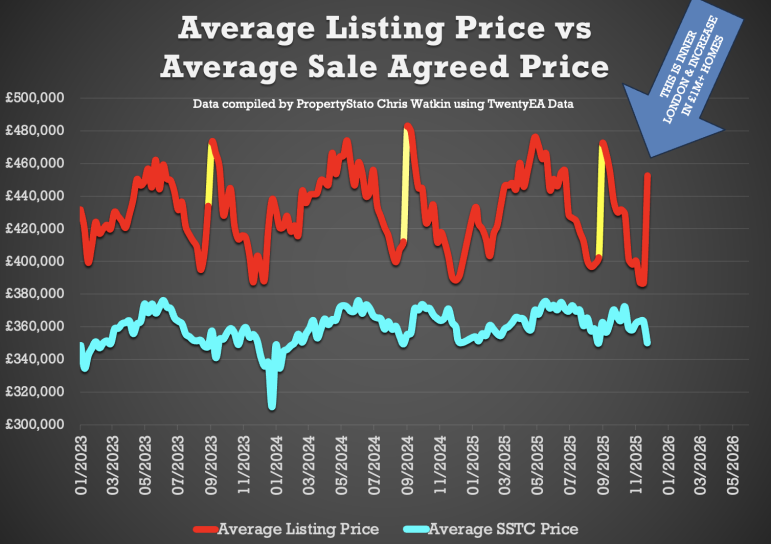

The one notable impact the funds has had is a big enhance in £1m+ listings in Interior London, bringing the typical itemizing value this week up by 20%+ on the final month’s common itemizing value.

Listings – 91% of Week 47 common

Gross Gross sales – 93% of Week 47 common

Web Gross sales – 94% of Week 47 common

(Week 47 common is predicated on the typical of the final 9 years)

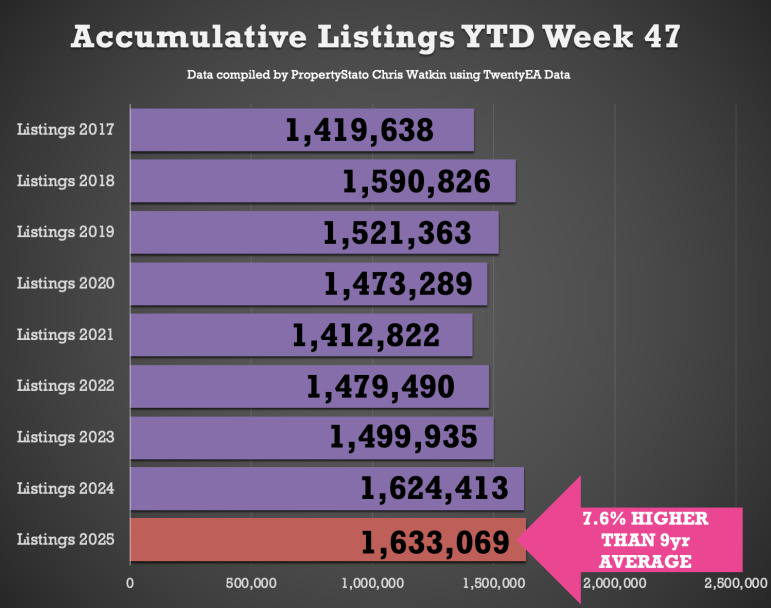

Listings – 1.633m YTD

Product sales – 1.203m YTD

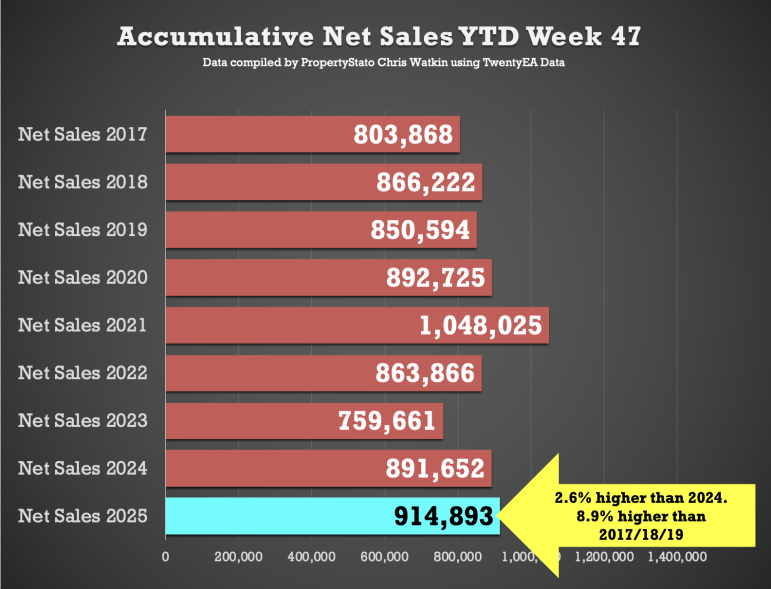

Web gross sales – 914k YTD

The complete breakdown …

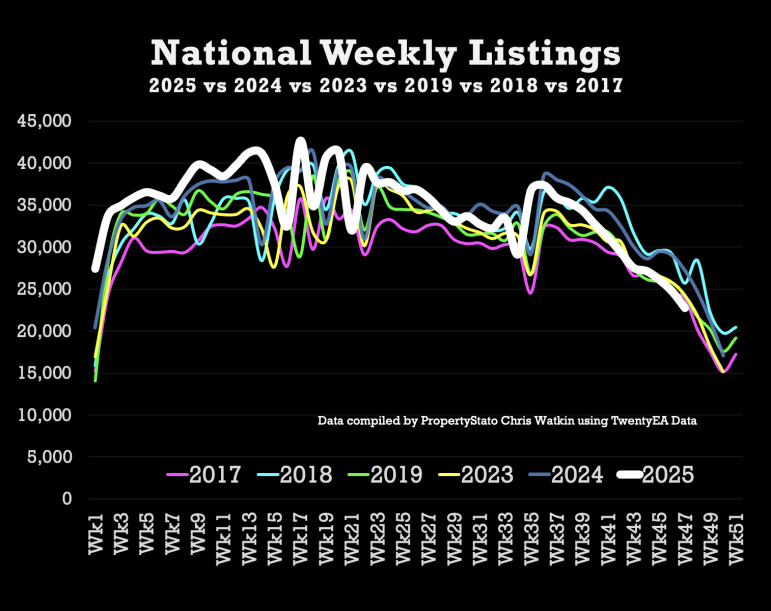

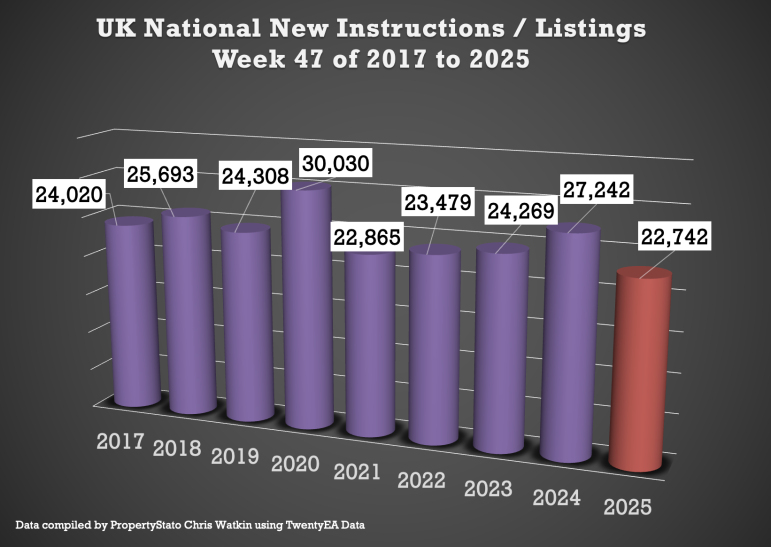

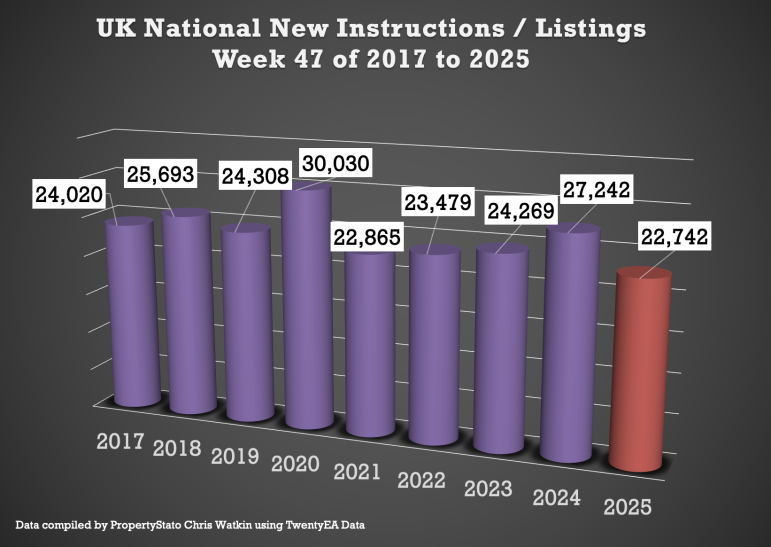

+ 22.7k new properties got here to market this week, down as anticipated from 24.7k final week.

+ 2025 weekly common: 34.7k.

+ 9 12 months week 47 common : 25k

+ 12 months-to-date (YTD): 1.633m new listings, 0.5% greater than 2024 YTD (1.624m) and eight.1% above the 2017–19 common (1.511m).

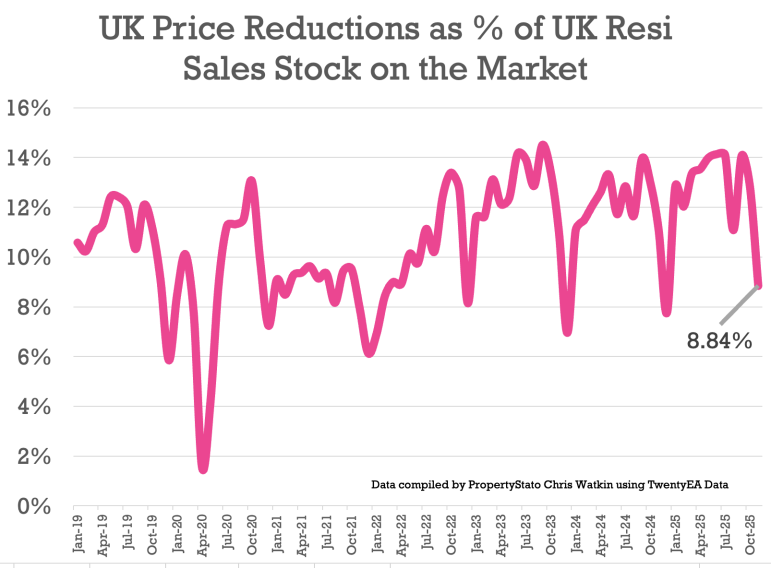

✅ Value Reductions

+ 13.2k reductions this week, decrease than final week’s at 13.4k (Property Brokers appear to neglect they’ll scale back homes costs after the primary week in November!). 23.2k is the typical weekly variety of reductions for 2025.

+ 8.8% of resi properties on the market had been decreased in November. In comparison with Oct 12.8%, Sept 14.1%, August 11.1%, July 14.1% in July and 14% in June.

+ 2025 common nonetheless stays at 12.8%, versus the five-year long-term common of 10.74%.

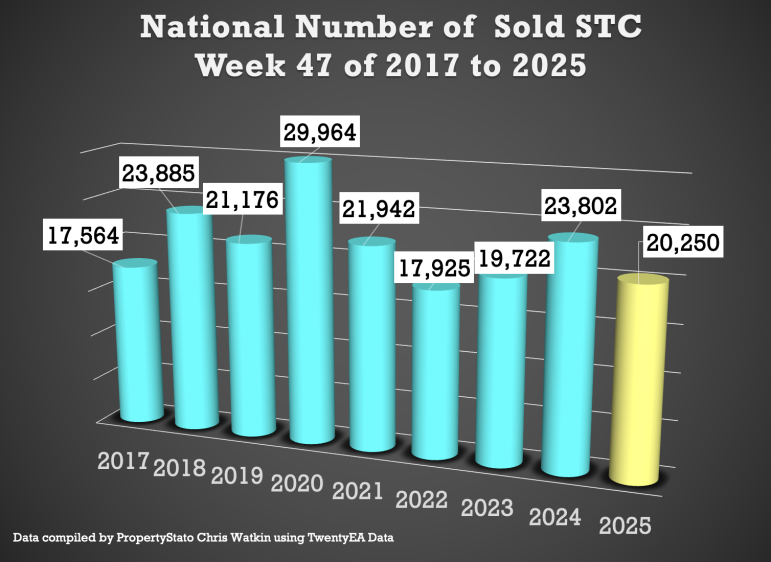

✅ Gross sales Agreed

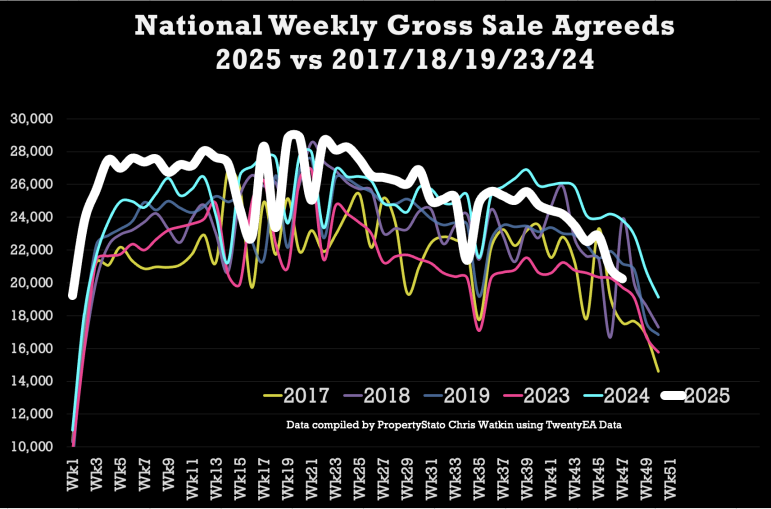

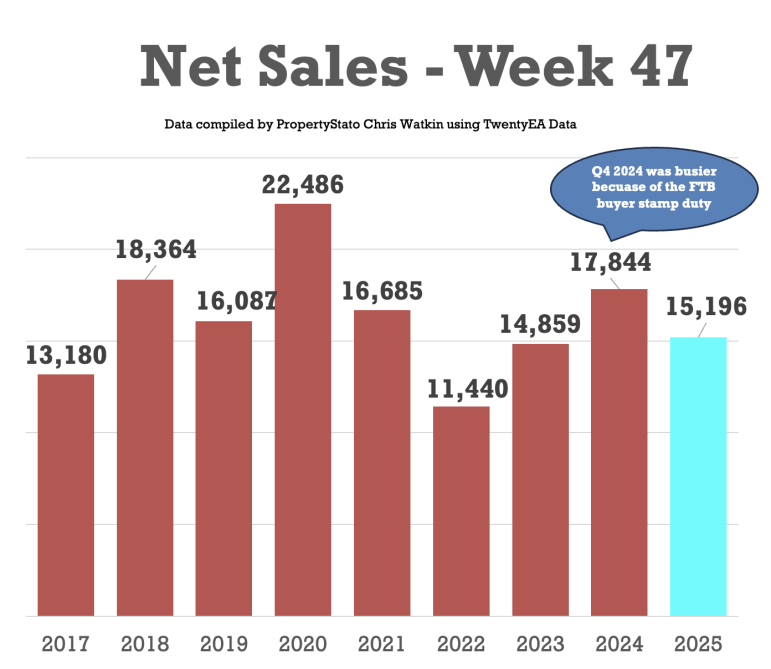

+ 20.3k properties offered topic to contract this week, down expectedly from 20.9k final week.

+ Week 47 common (for final 9 years) :21.8k

+ 2025 weekly common : 26k.

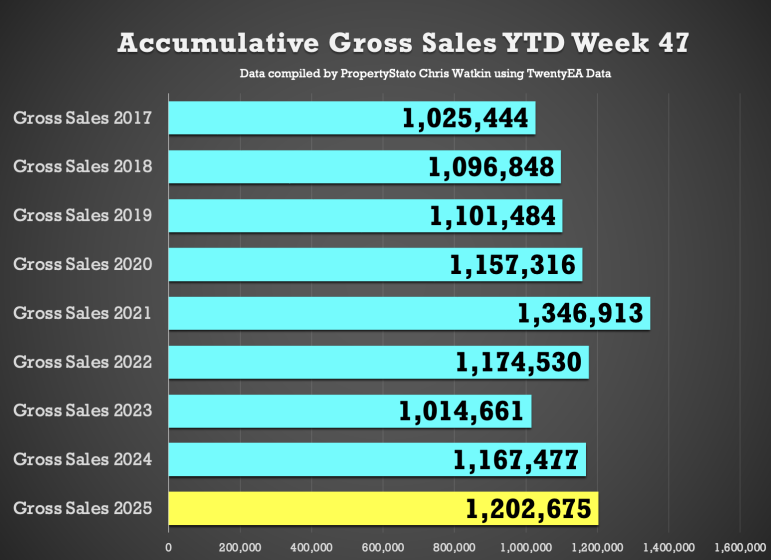

+ YTD: 1.203m product sales, which is 3% forward of 2024 (1.167m) and 11.9% above the 2017–19 common (1.074m).

+ Some will observe Gross Gross sales in This autumn had been greater – this was the primary time consumers had been shopping for properties to beat the March 2025 stamp responsibility deadline.

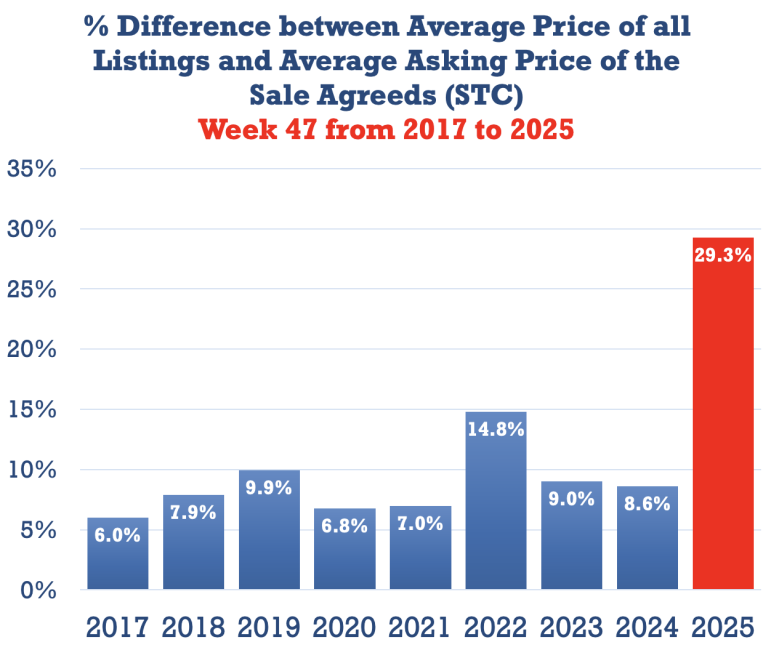

✅ Value Diff between Listings & Gross sales

+ Common Asking Value of listings final week £452k vs (£395 for the month earlier than). This a large leap and is right down to numerous Interior London residence sin the £1.5m+ coming available on the market.

+ Common asking value of Gross sales Agreed (SSTC)final week was £350k (in keeping with the typical of 2025) – a29.3% distinction (long run 9 12 months common is 16% to 17%.

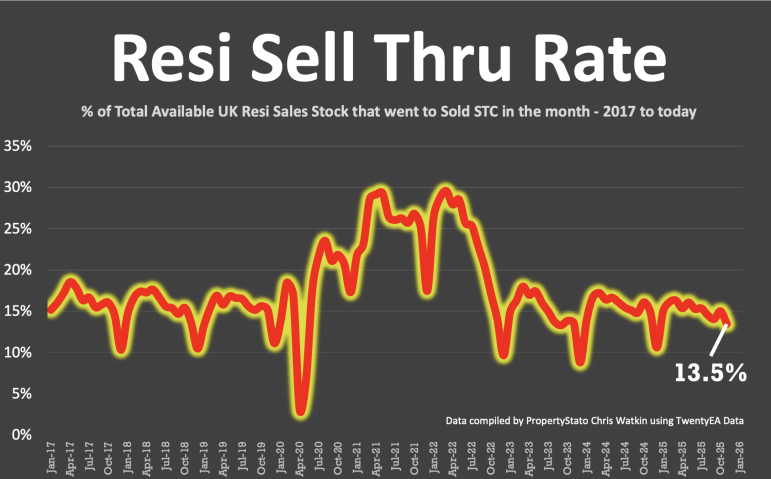

✅ Promote-By Price

+ 13.5% of properties on brokers’ books went SSTC in October. Down from 15% in October, 14.1% in Sept, 14.5% in Aug, 15.4% in July, 15.3% in June, and 16.1% in Could.

+ Pre-Covid common: 15.5%.

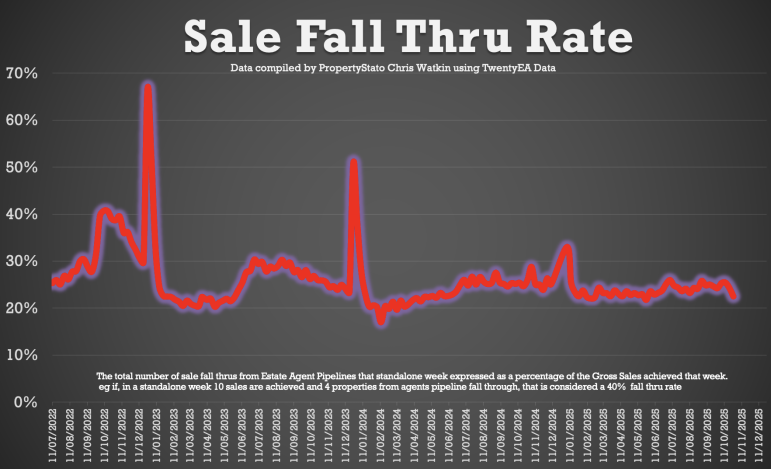

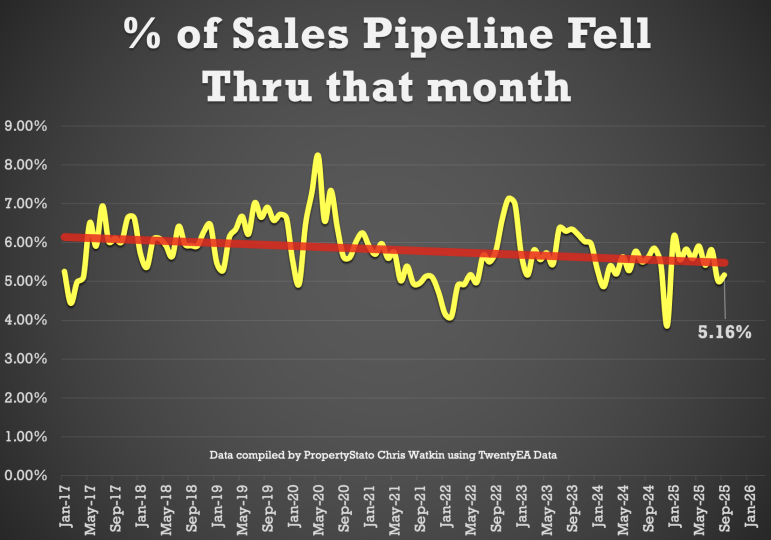

✅ Fall-Throughs

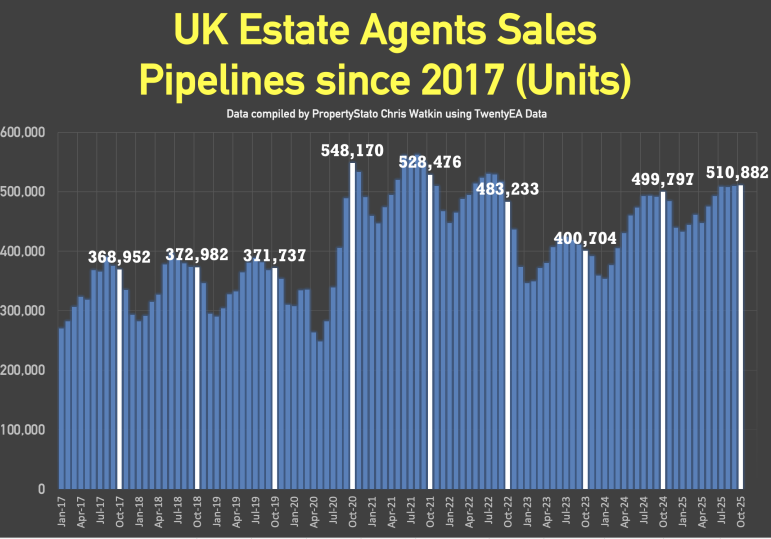

+ 5,054 fall-throughs final week (pipeline of 510k residence Offered STC).

+ Weekly common for 2025: 6,128.

+ Fall-through price: 25%, barely up from 24.7% final week.

+ Lengthy-term common: 24.2% (post-Truss chaos noticed ranges exceed 40%).

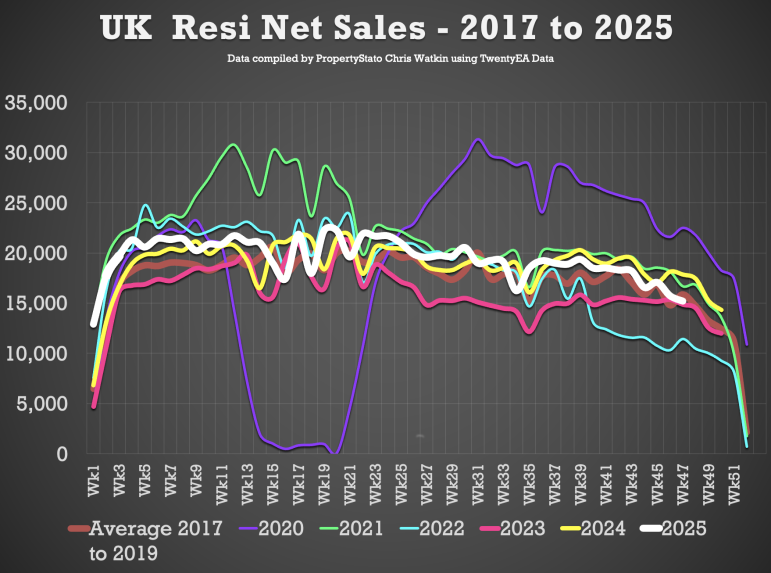

✅ Web Gross sales

+ 15.2k web gross sales this week, down expectedly from 15.7k final week.

+ 9-year Week 47 common: 16.2k.

+ Weekly common for 2025: 19.4k.

+ YTD: 914k, which is 2.6% forward of 2024 (892k) and 9.1% above 2017–19 (840k).

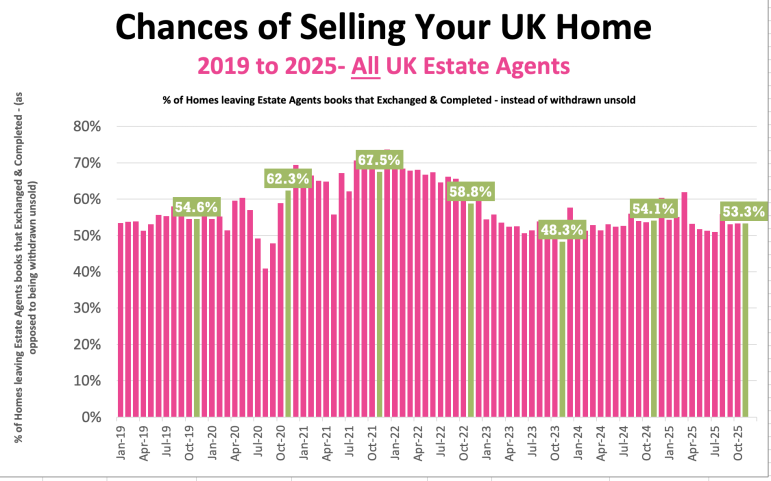

✅ Chance of Promoting (% that Trade vs withdrawal)

+ November Stats : 53.3% of properties that left brokers’ books exchanged & accomplished in November. (Notice this determine will change all through the month as extra November stats are available in). (49.7k exchanges & 43.6k withdrawals as at third Dec 2025)

+ October 53.3% / September: 53.1% / August :55.8% / July: 50.9% / June: 51.3% / Could: 51.7% / April: 53.2%.

✅ Inventory Ranges

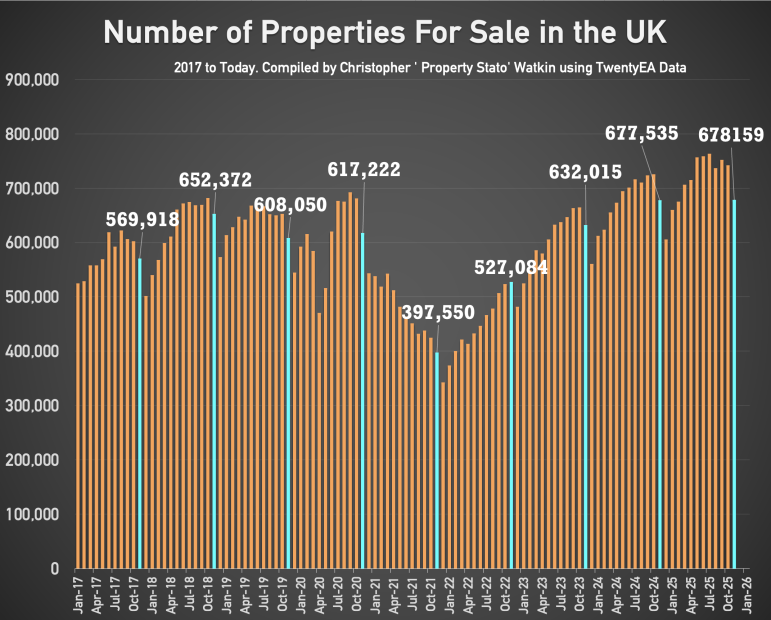

+ 678k properties available on the market on the first of December, down from 742k on 1st of November. December ’25 is equivalent to December ’24.

+ 511k properties in gross sales pipeline on the first November, 2.2% greater than 12 months in the past. (1st December figures to comply with in subsequent week’s present).