Home costs are anticipated to document modest development over the approaching years, rising by 2.5% throughout Nice Britain by the fourth quarter of 2026 as cooling inflation and easing rates of interest assist the market, in accordance with the newest housing market outlook from Hamptons.

The property company forecasts that transaction volumes are more likely to maintain regular at round 1.15 million in 2026, with bettering affordability balancing ongoing financial and tax pressures.

From 2027, nonetheless, political uncertainty and better borrowing prices are set to weigh extra closely in the marketplace, slowing value development to 2.0% in late 2027 and 1.5% by the tip of 2028. Prime markets are more likely to stay subdued, with tax coverage and broader uncertainty limiting mobility and delaying restoration.

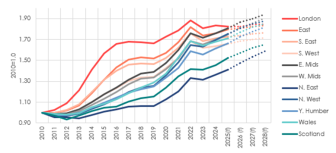

Notably, by subsequent yr the East Midlands is projected to have seen better value development because the 2009 market backside than London, with the North West and West Midlands anticipated to comply with by the tip of 2027 – signalling a major shift within the regional home value cycle.

Annual home value development forecast

| This autumn 2024 | This autumn 2025 (f) | This autumn 2026 (f) | This autumn 2027 (f) | This autumn 2028 (f) | 4

yr complete (2024-28) |

|

| London | 1.5% | -0.5% | 0.0% | 1.0% | 0.0% | 0.5% |

| East of England | 1.2% | 2.0% | 0.5% | 1.0% | 0.5% | 4.1% |

| South East | 1.6% | 1.0% | 0.5% | 1.0% | 0.5% | 3.0% |

| South West | 1.0% | 1.5% | 1.5% | 1.0% | 1.0% | 5.1% |

| East Midlands | 2.3% | 3.0% | 3.0% | 2.0% | 2.0% | 10.4% |

| West Midlands | 2.9% | 3.0% | 3.5% | 2.5% | 2.5% | 12.0% |

| North East | 3.9% | 3.5% | 4.5% | 4.0% | 3.5% | 16.4% |

| North West | 3.9% | 3.5% | 3.0% | 2.5% | 1.5% | 10.9% |

| Yorkshire & Humber | 3.8% | 3.0% | 4.0% | 2.5% | 2.5% | 12.5% |

| Wales | 2.1% | 2.0% | 3.5% | 2.5% | 2.0% | 10.4% |

| Scotland | 3.1% | 5.0% | 3.0% | 3.0% | 2.0% | 13.6% |

| Nice Britain | 2.4% | 2.0% | 2.5% | 2.0% | 1.5% | 8.2% |

Supply: ONS & Hamptons

Hamptons predicts that inflation is more likely to fall sooner than anticipated subsequent yr, permitting for 2 or three base price cuts. It additionally expects the Financial institution Charge to settle at round 3.25% by the tip of 2026, with typical mortgage charges stabilising at round 4.0%. This could enhance the supply of sub-4% mortgage offers, even for debtors with smaller deposits, serving to to assist value development and exercise.

Affordability is bettering on paper, with earnings development operating forward of inflation. Whereas some households rolling off shorter fixed-rate offers are seeing decrease month-to-month funds, others are nonetheless adjusting to greater prices. There are round 600,000 debtors on ultra-low sub-3% five-year fixes who’ll be rolling off in 2026 and 2027.

London & prime markets – a restoration delayed

At this stage within the cycle, Hamptons would sometimes anticipate the London market to regain momentum. Traditionally, the capital leads recoveries as soon as affordability improves, however this time the rebound appears to be like muted.

Since 2016, London has persistently underperformed the remainder of Nice Britain, and our forecasts counsel that development will proceed – a reversal of what we beforehand anticipated (chart 1). The company anticipate flat development (0.0%) throughout Better London in 2026 because the market digests latest tax adjustments (desk 1).

Whereas small value falls are anticipated within the £1.9m+ phase, that is more likely to be offset by development within the mainstream market, the place bettering affordability and easing mortgage charges are beginning to assist purchaser confidence.

One rising problem is the dearth of value development for higher-value properties. Declining costs – significantly in Prime Central London – imply a rising share of households are promoting for lower than they paid. In 2025, 14% of London sellers offered at a loss, up from 6% in 2016. This disincentivises strikes and encourages house owners to remain put, particularly when confronted with the excessive value of Stamp Obligation Land Tax on their subsequent buy.

In consequence, the London market is more and more being pushed by first-time patrons, who accounted for 50% of properties offered within the capital this yr.

The choice to boost Stamp Obligation Land Tax earlier this yr – mixed with wider tax considerations, together with adjustments to non-dom standing and hypothesis round capital positive factors and inheritance tax – has created a difficult backdrop for high-value markets. The brand new council tax surcharge on properties value over £2 million provides one other layer of value, additional dampening sentiment and subsequently values.

Prime Nation markets, the place council tax payments are already considerably greater than in London, may come beneath even better strain from this surcharge. These areas noticed sturdy development post-Covid, however political uncertainty and tax burdens at the moment are prompting many households to delay transferring. Properties above the £2m mark may see round a 5% value correction, however that is anticipated to be a one-off adjustment fairly than a protracted decline, as markets take up the change and stabilise. Tax charges stay under European and US equivalents.

2027–2028: The next inflation period and political threat

It appears to be like more and more probably that 2026 will mark the tip of the rate-cut cycle, and the years forward look extra unsure too, in accordance with Hamptons. Inflation is predicted to stay above the two% goal, and mortgage charges may start to edge greater in 2027 as markets start to think about future rate of interest will increase. Towards this backdrop, home value development throughout Nice Britain is forecast to sluggish to round 2.0% in This autumn 2027 and 1.5% in This autumn 2028.

Political uncertainty will grow to be a extra distinguished driver of sentiment, significantly in prime markets in 2028 – the yr earlier than the deliberate election. Tax coverage is more and more appearing as a levelling-up mechanism, limiting restoration in higher-value markets in London and the South.

London is forecast to see round 1.0% development in 2027, earlier than stalling once more in 2028. The rising burden of stamp responsibility and different levies will proceed to dampen exercise.

In actual phrases (i.e. inflation-adjusted), home costs are more likely to proceed underperforming, with affordability stretched and uneven earnings development. Whereas headline wage development could stay sturdy – pushed partly by fewer entry-level roles – the advantages won’t be evenly distributed. This may significantly influence first-time patrons and renters.

Over the four-year forecast interval, the North East is ready to see the strongest development (16.4%), adopted by Scotland (13.6%) and Yorkshire & The Humber (12.5%). These areas have seen a few of the weakest development since 2010, so this acceleration marks a catch-up part.

Cumulative home value development throughout the areas since 2010

Supply: ONS & Hamptons

Whereas London has traditionally been the secure wager for long-term value development, the image is altering. Since This autumn 2010, when home costs bottomed out, costs in London have risen by 84%, outperforming each different area and the Nice Britain common of 74% (chart 1). However subsequent yr may mark a turning level: the East Midlands is forecast to overhaul London in cumulative development, with the North West and West Midlands following by the tip of 2027 (chart 1).

By 2028, Hamptons anticipate costs throughout Nice Britain to have risen by 84% since 2010 (chart 1). The East Midlands would be the high performer over the interval (94%), adopted by the West Midlands (90%) and the North West (88%). London will fall to fourth place and would be the solely area the place common costs stay under their 2022 peak. This shift displays stronger affordability and financial resilience in these areas in contrast with the capital.

Transaction volumes are forecast to rise barely to 1.2 million throughout Nice Britain in 2027, earlier than dipping again to 1.15 million in 2028 as political uncertainty forward of the 2029 election results in a pause, significantly in prime markets (desk 2). General, the market is predicted to grow to be more and more sentiment-driven, with volatility round key political occasions.

Transactions forecast

| 2024 | 2025(f) | 2026(f) | 2027(f) | 2028(f) |

| 1,076,970 | 1,150,000 | 1,150,000 | 1,200,000 | 1,150,000 |

Supply: HMRC & Hamptons

Property transactions versus development within the complete variety of households

Supply: HMRC & Hamptons

On the similar time, persons are transferring much less usually – and making larger, extra “future-proofed” strikes after they do. Regardless of there being 10% extra owner-occupied households in England since 2008, transaction numbers stay round 19% under the common stage seen within the three years earlier than the 2008 monetary crash (chart 2).

With out right this moment’s vital tax obstacles, Hamptons provides that it will anticipate round an additional 100,000 strikes annually. If stamp responsibility have been eradicated totally, transaction volumes may frequently surpass 1.4 million yearly, much like the post-pandemic peak in 2021.