Welcome to the thirty ninth UK Property Market Stats Present of 2025, your weekly TV programme on the UK housing market.

This week, I’m joined by Kristian Stott, a number one former property agent and now PropTech guru, as we unpack the important thing headlines from week ending Sunday fifth October 2025).

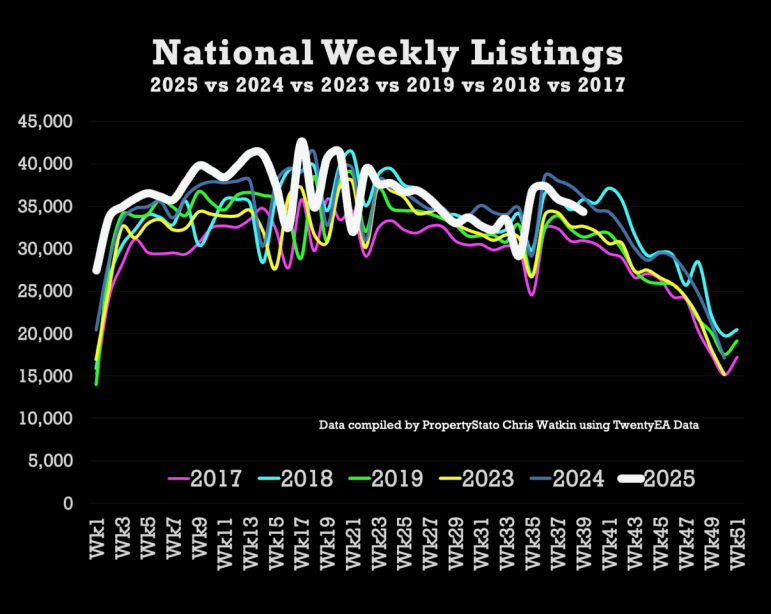

✅ New Listings

34.3k new properties got here to market this week, down as anticipated from 35.3k final week.

2025 weekly common: 36.2k.

9 12 months week 39 common :34.3k

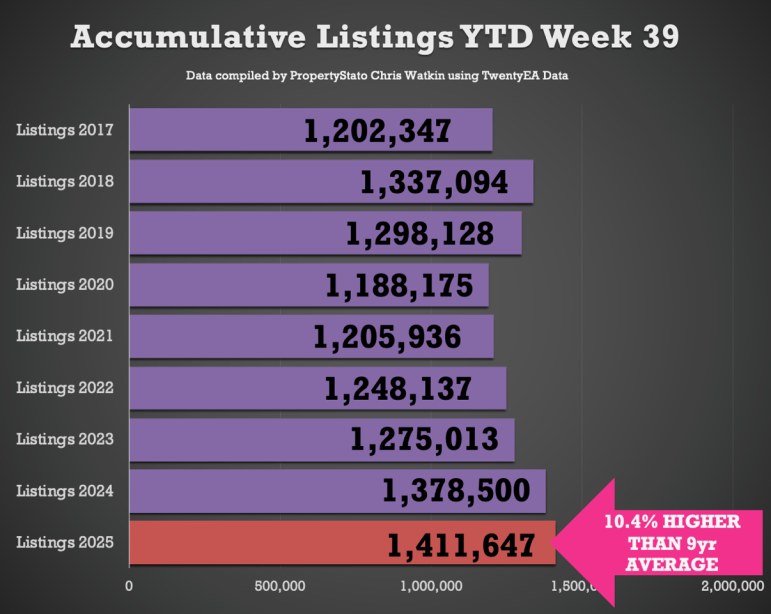

Yr-to-date (YTD): 1.41m new listings, 2.4% greater than 2024 YTD (1.38m) and 10% above the 2017–19 common (1.28m).

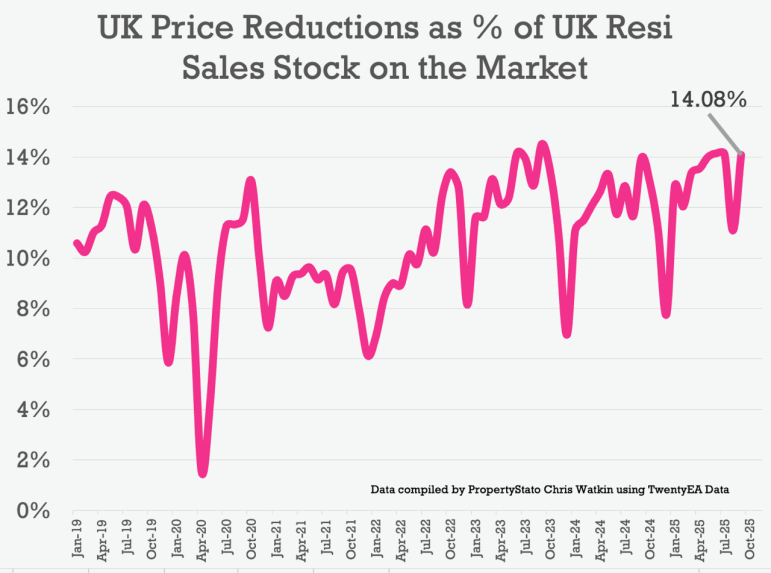

✅ Value Reductions

25.6k reductions this week, barely greater to final week at 25k.

Improve within the variety of properties in the marketplace being lowered in September to 14.1%. In August, it was 11.1% (everybody will need to have been on vacation!), while it was 14.1% in July and 14% in June.

2025 common up to now: 13.2%, versus the five-year long-term common of 10.74%.

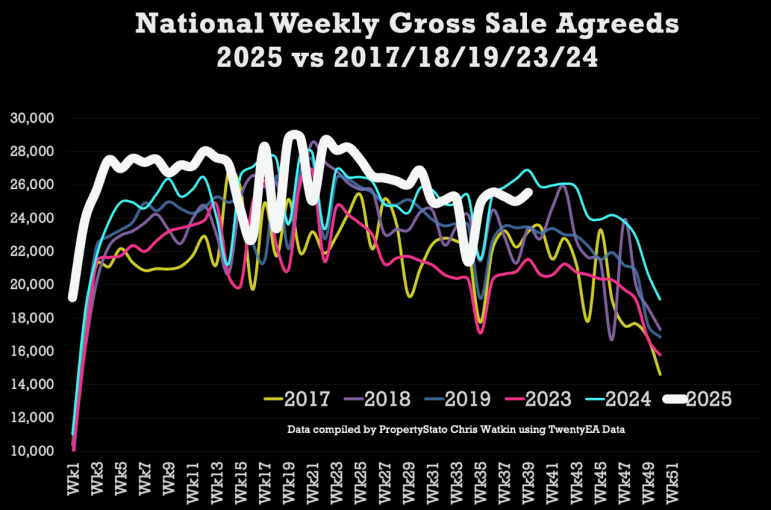

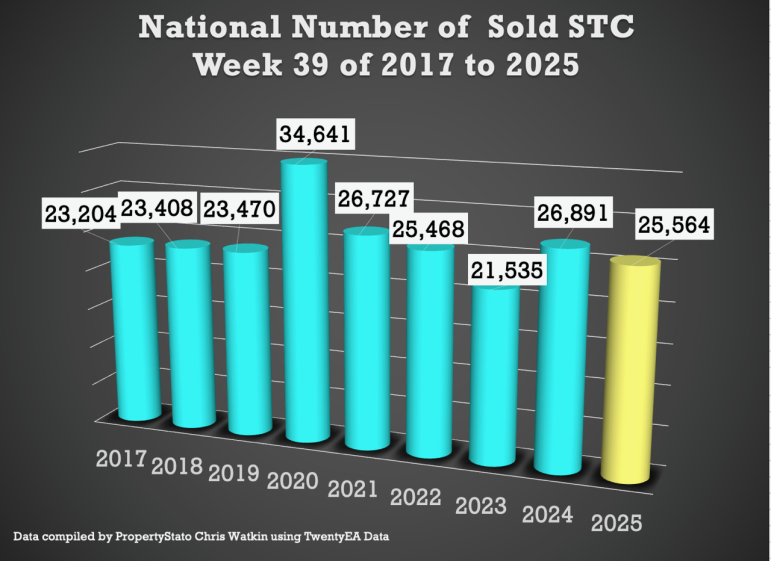

✅ Gross sales Agreed

25.6k properties bought topic to contract this week, up from 25k final week.

Week 39 common (for final 9 years) :25.7k

2025 weekly common : 26.1k.

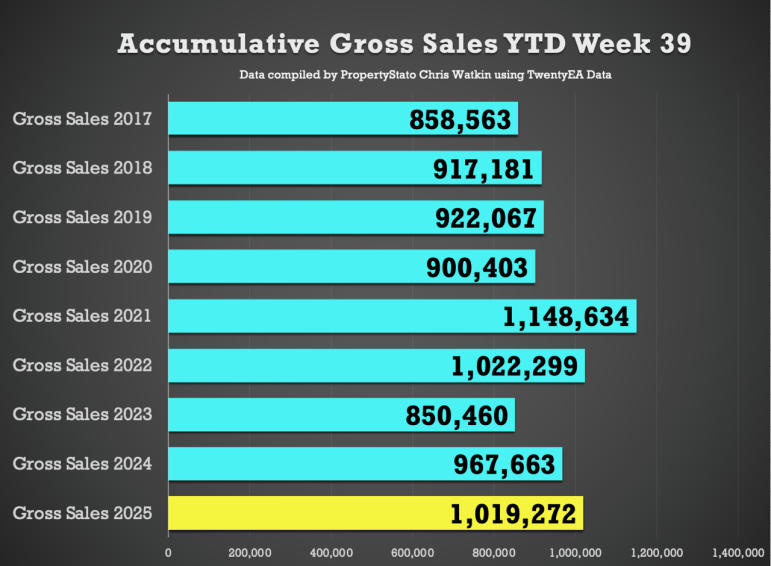

YTD: 1.019m product sales, which is 5.3% forward of 2024 (968k) and 13.3% above the 2017–19 common (899k).

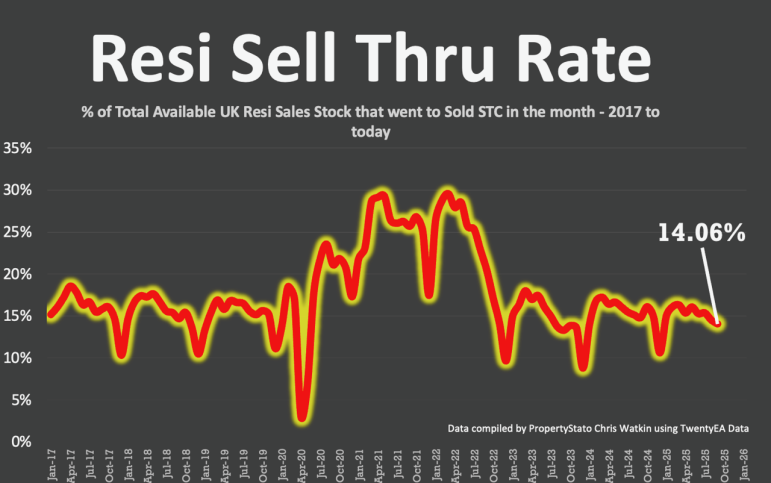

✅ Promote-Via Price

14.1% of properties on brokers’ books went SSTC in September.

Down from 14.5% in Aug, 15.4% in July, 15.3% in June, and 16.1% in Might.

Pre-Covid common: 15.5%.

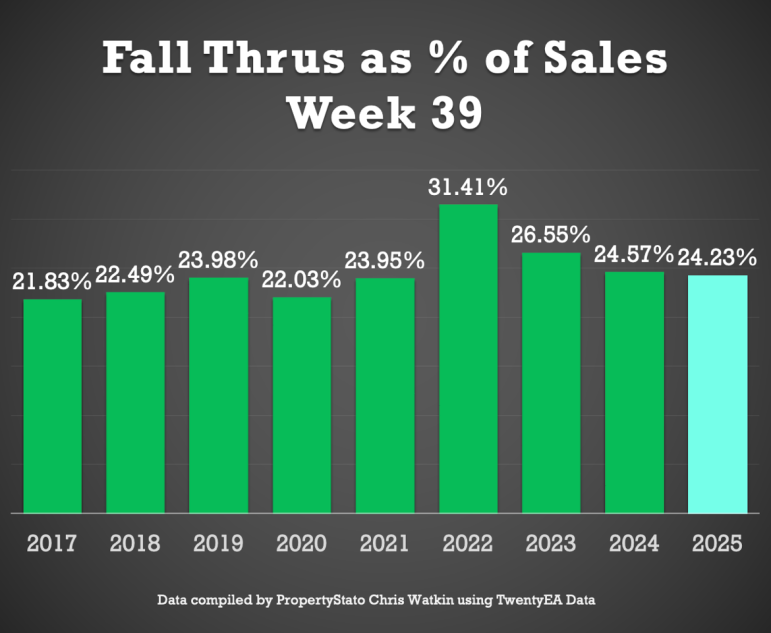

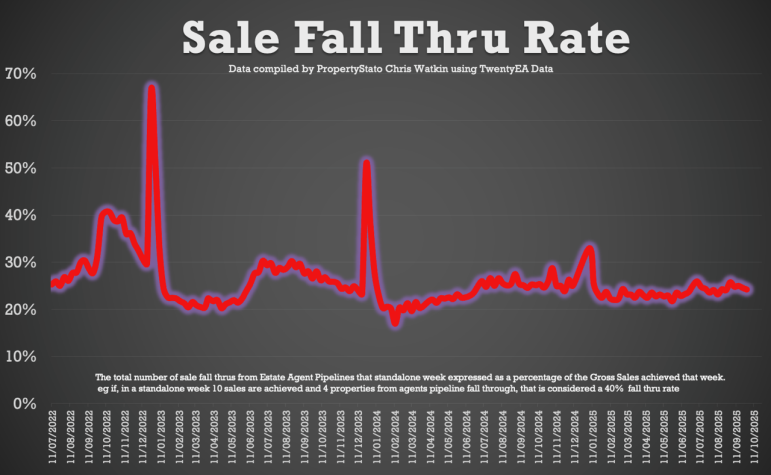

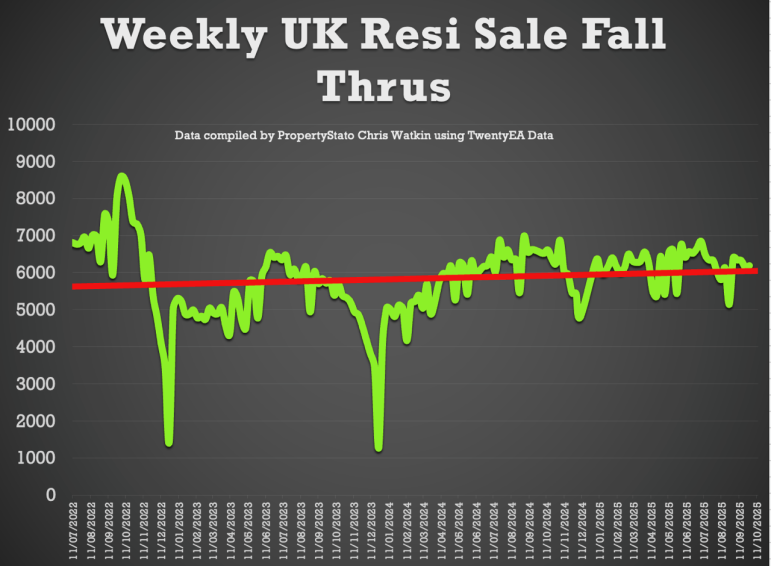

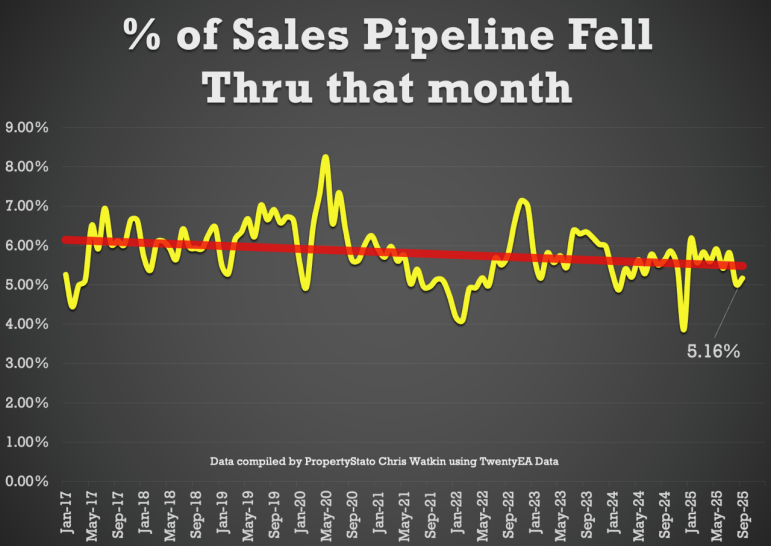

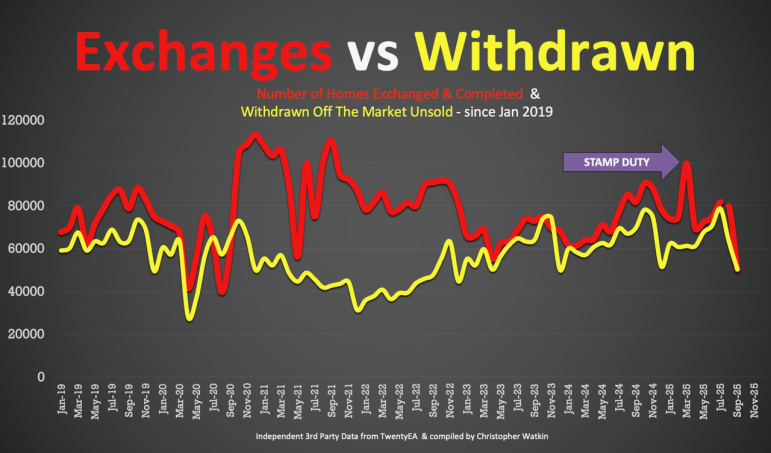

✅ Fall-Throughs

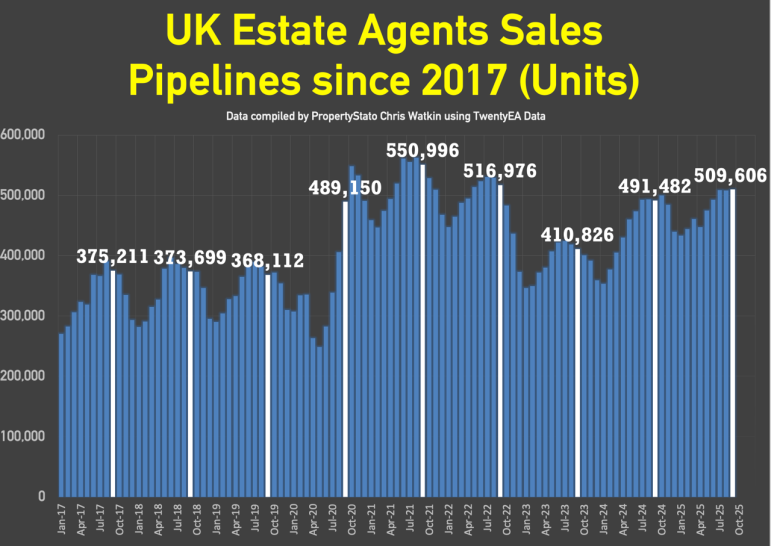

6,149 fall-throughs final week (pipeline of 510k dwelling Bought STC).

Weekly common for 2025: 6,217.

Fall-through fee: 24.6%, down from 25% final week.

Lengthy-term common: 24.2% (post-Truss chaos noticed ranges exceed 40%).

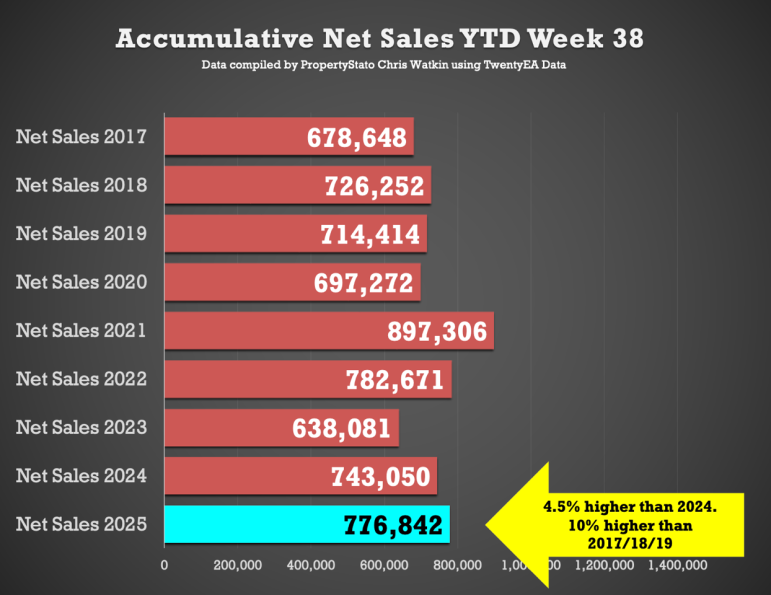

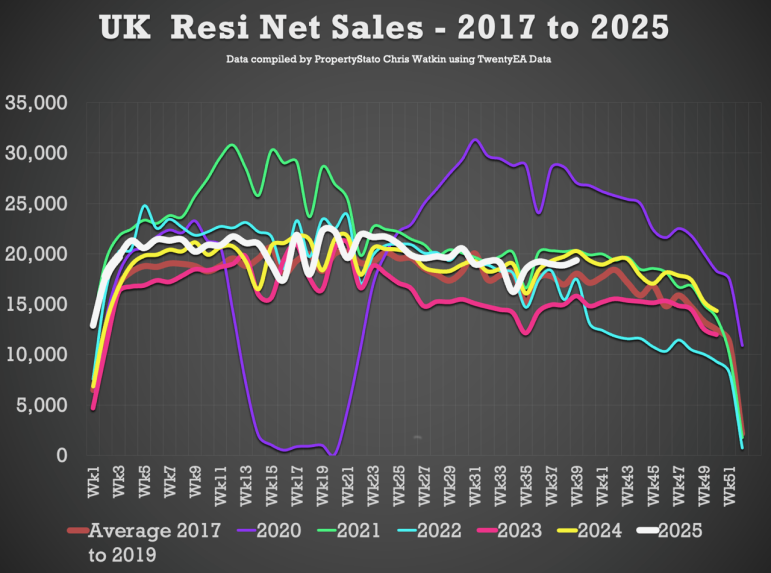

✅ Internet Gross sales

19.4k web gross sales this week, up from 18.9k final week.

9-year Week 39 common: 19.4k.

Weekly common for 2025: 19.9k.

YTD: 777k, which is 4.5% forward of 2024 (743k) and 10% above 2017–19 (706k).

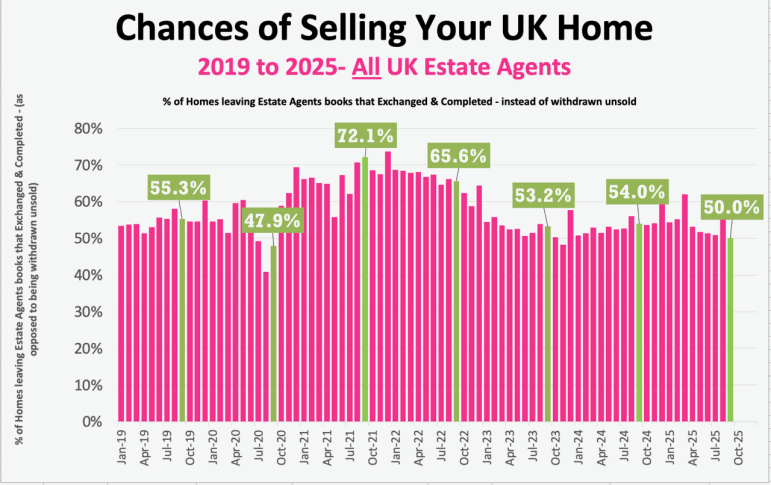

✅ Likelihood of Promoting (% that Alternate vs withdrawal)

Preliminary September Stats : 50% of properties that left brokers’ books exchanged & accomplished. (Notice it will change as extra September stats are available in all through October)

August :55.8% / July: 50.9% / June: 51.3% / Might: 51.7% / April: 53.2%.

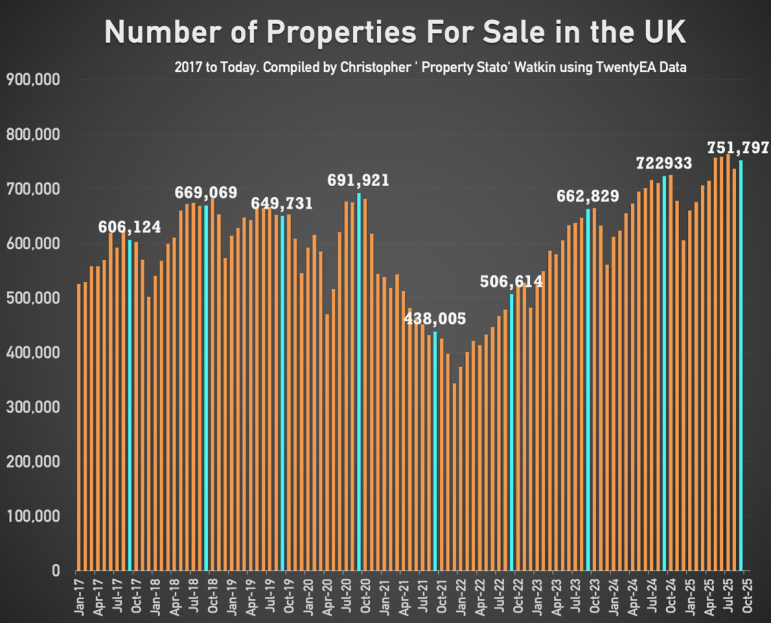

✅ Inventory Ranges

751k properties in the marketplace firstly of October, 4% greater than October 2024. (723k)

510k properties in gross sales pipeline on the first October, 2% greater than 12 months in the past.

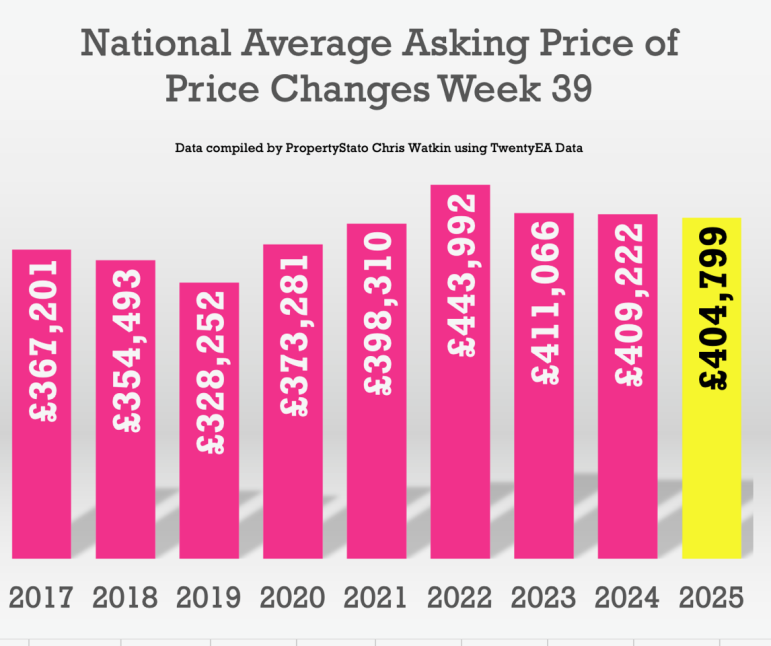

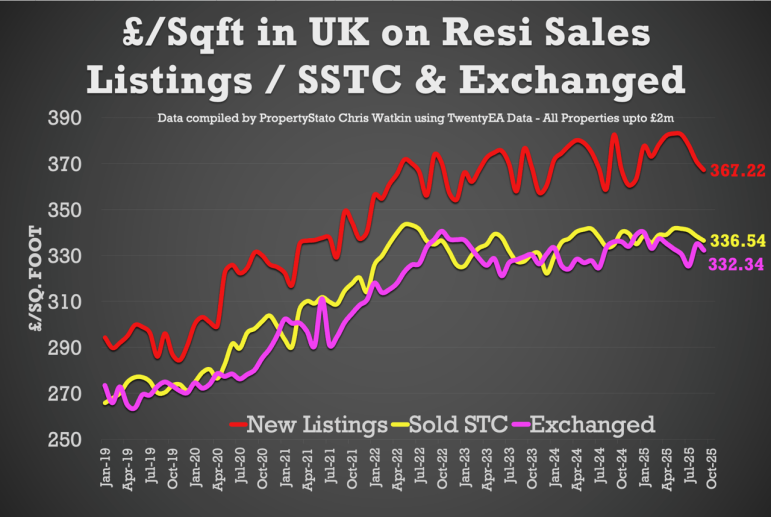

✅ Home Costs (£/sq.ft)

October 2025 agreed gross sales averaged £336.54 per sq.ft.

✅ Native Concentrate on the Present:

St Albans

✅ Summer time Evaluation of London vs remainder of the UK

⭕ January to July 2025

London

• Common asking worth of recent listings, £946k

• Common worth of gross sales agreed, £769k

• Weekly averages, listings 3,195, gross sales agreed 1,508

• Gross sales-agreed to listings ratio, 47.2%

Remainder of UK, excluding London

• Common asking worth of recent listings, £394k

• Common worth of gross sales agreed, £341k

• Weekly averages, listings 33,622, gross sales agreed 25,034

• Gross sales-agreed to listings ratio, 74.5%

⭕ August and September 2025

London

• Common asking worth of recent listings, £921k

• Common worth of gross sales agreed, £760k

• Weekly averages, listings 2,993, gross sales agreed 1,222

• Gross sales-agreed to listings ratio, 40.8%

Remainder of UK, excluding London

• Common asking worth of recent listings, £381k

• Common worth of gross sales agreed, £339k

• Weekly averages, listings 31,108, gross sales agreed 23,462

• Gross sales-agreed to listings ratio, 75.4%

⭕ What modified in Aug–Sep versus Jan–Jul

London

• Gross sales-agreed to listings ratio down 6.4 proportion factors

• Gross sales agreed per week down 19.0%

Remainder of UK

• Gross sales-agreed to listings ratio up 0.9 proportion factors

• Gross sales agreed per week down 6.3%

⭕ What it means

Volumes softened all over the place in late summer time, nevertheless London’s fall in gross sales agreed was a lot bigger, and its conversion from listings to gross sales slipped additional. The remainder of the UK held conversion regular and guarded extra of its gross sales quantity. Clear late-summer divergence.