Myself and Toby Martin from We Are Unchained assessment exercise in Week 48 of the UK property market, masking the seven days to Sunday 7 December 2025.

✅ New Listings

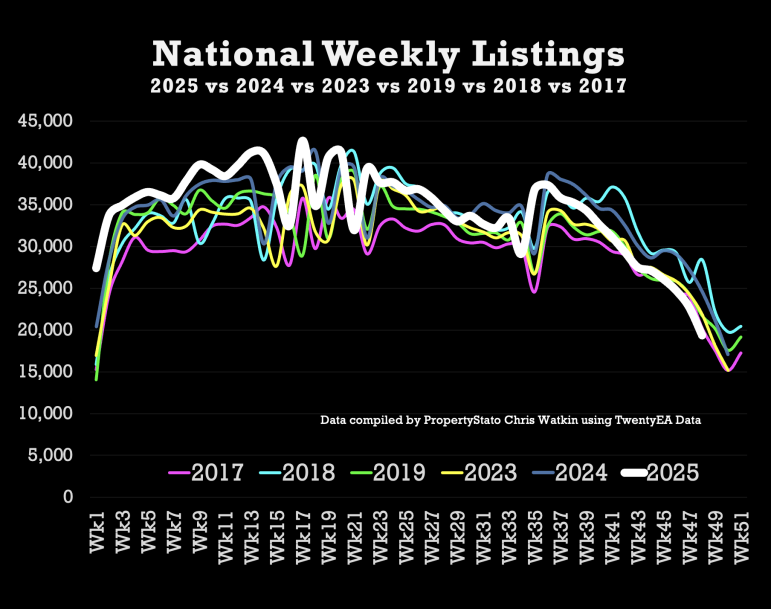

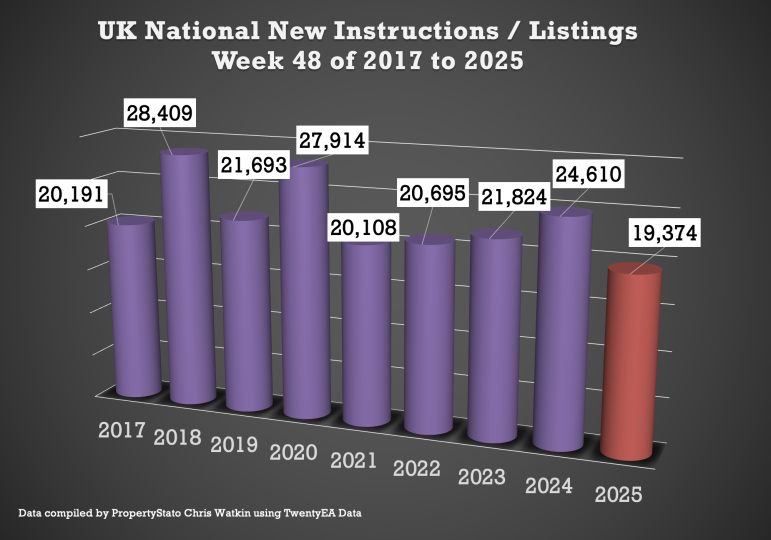

+ 19.4k new properties got here to market this week, down as anticipated from 22.7k final week.

+ 2025 weekly common: 34.4k.

+ 9-year week 48 common : 22.8k

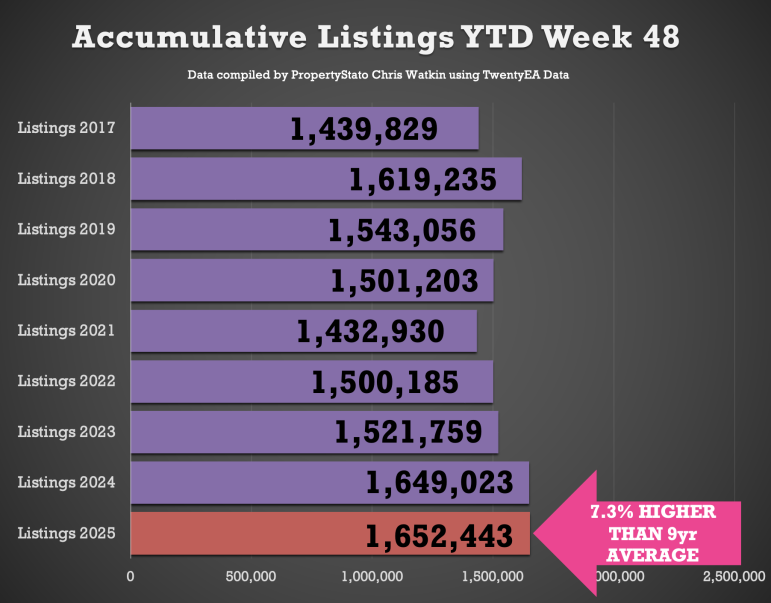

+ Yr-to-date (YTD): 1.652m new listings, 0.2% increased than 2024 YTD (1.649m) and seven.7% above the 2017–19 common (1.534m).

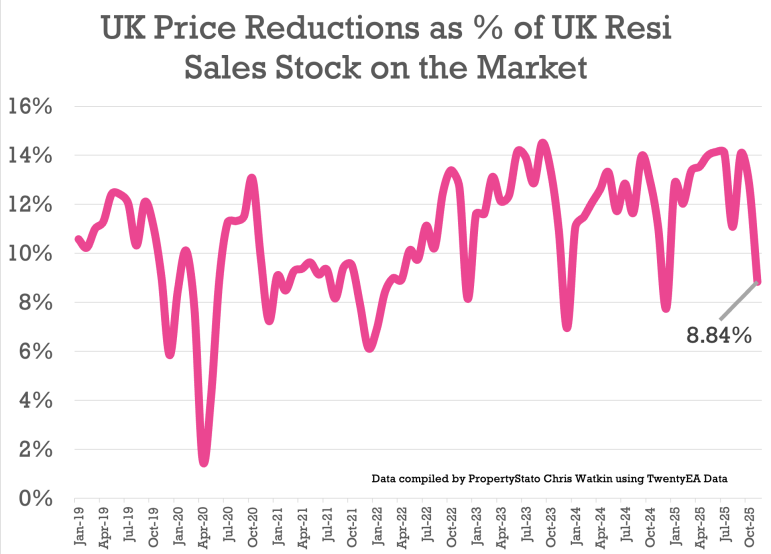

✅ Value Reductions

+ 12.8k reductions this week, decrease than final week’s at 13.2k (Property Brokers appear to neglect they’ll cut back homes costs after the primary week in November!). 23.2k is the typical weekly variety of reductions for 2025.

+ 8.8% of resi properties on the market had been lowered in November. In comparison with Oct 12.8%, Sept 14.1%, August 11.1%, July 14.1% in July and 14% in June.

+ 2025 common nonetheless stays at 12.8%, versus the five-year long-term common of 10.74%.

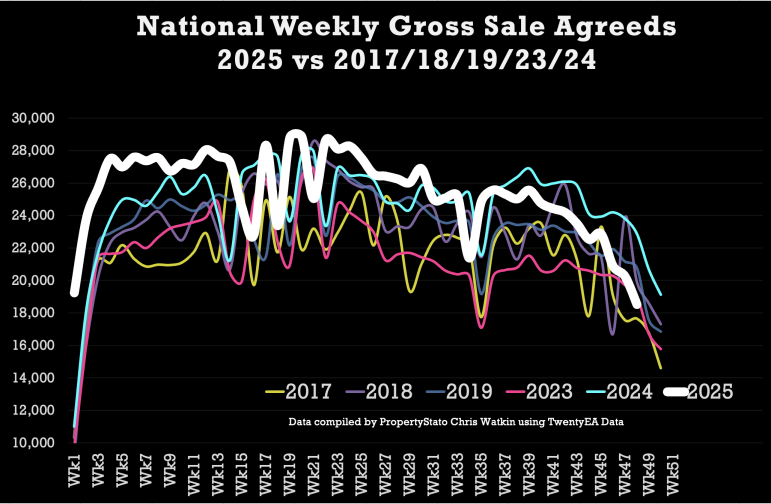

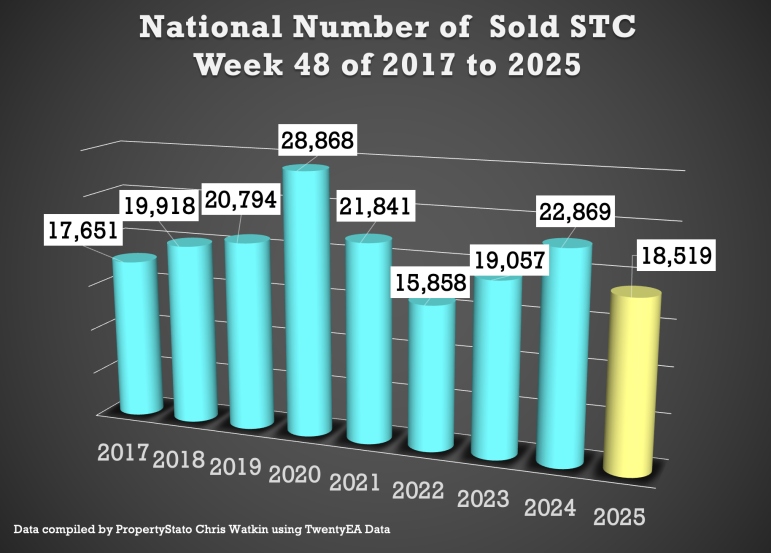

✅ Gross sales Agreed

+ 18.5k properties bought topic to contract this week, down expectedly from 20.3k final week.

+ Week 48 common (for final 9 years) : 20.6k

+ 2025 weekly common : 25.4k.

+ YTD: 1.221m product sales, which is 2.6% forward of 2024 (1.190m) and 11.6% above the 2017–19 common (1.094m).

+ Some will word Gross Gross sales in This autumn had been increased – this was the primary time consumers had been shopping for properties to beat the March 2025 stamp obligation deadline.

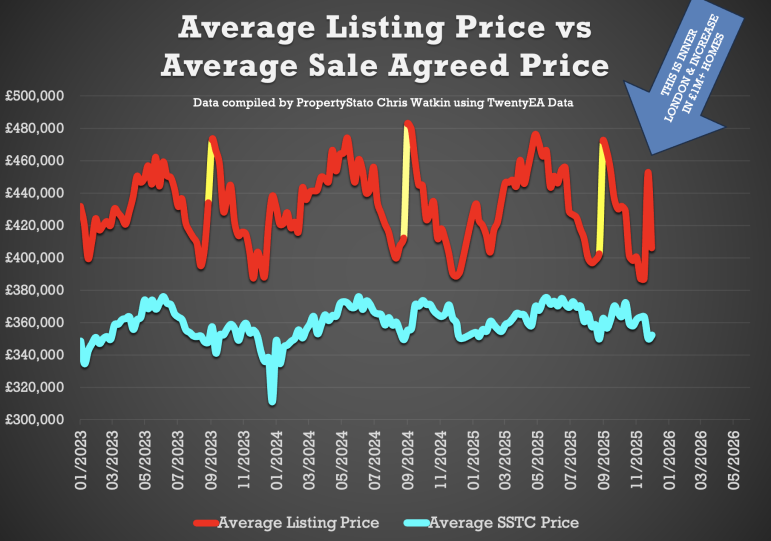

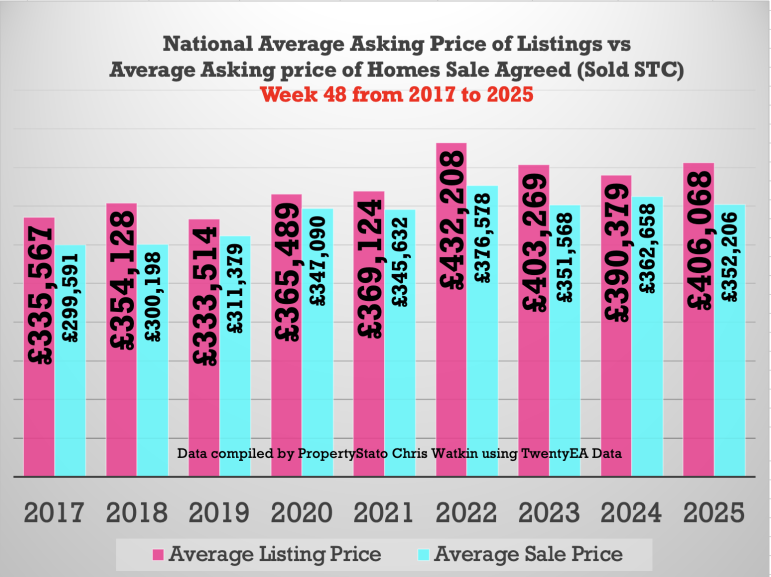

✅ Value Diff between Listings & Gross sales

+ Common Asking Value of listings final week £406k

+ Common asking worth of Gross sales Agreed (SSTC) final week was £352k

+ A 15.3% distinction (long run 9 yr common is 16% to 17%).

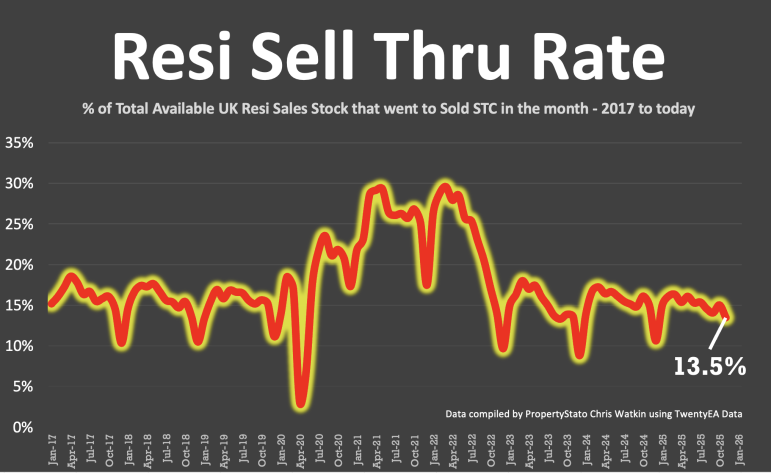

✅ Promote-By Price

+ 13.5% of properties on brokers’ books went SSTC in November. Down from 15% in October, 14.1% in Sept, 14.5% in Aug, 15.4% in July, 15.3% in June, and 16.1% in Could.

+ Pre-Covid common: 15.5%.

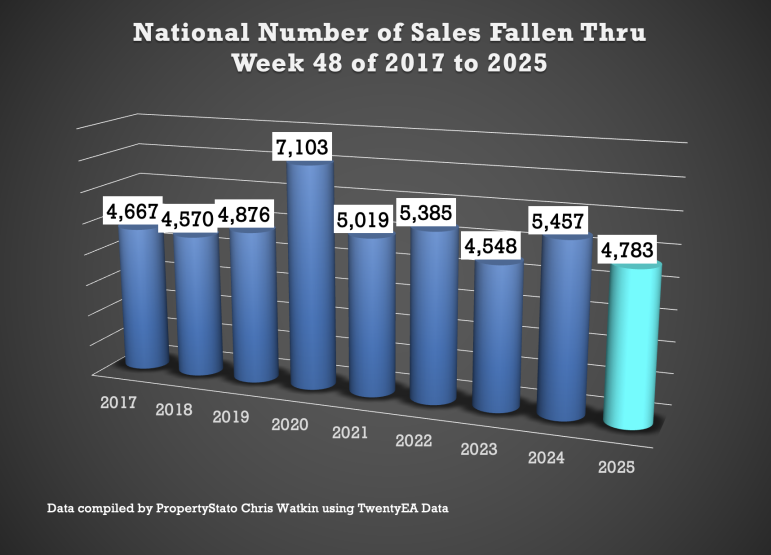

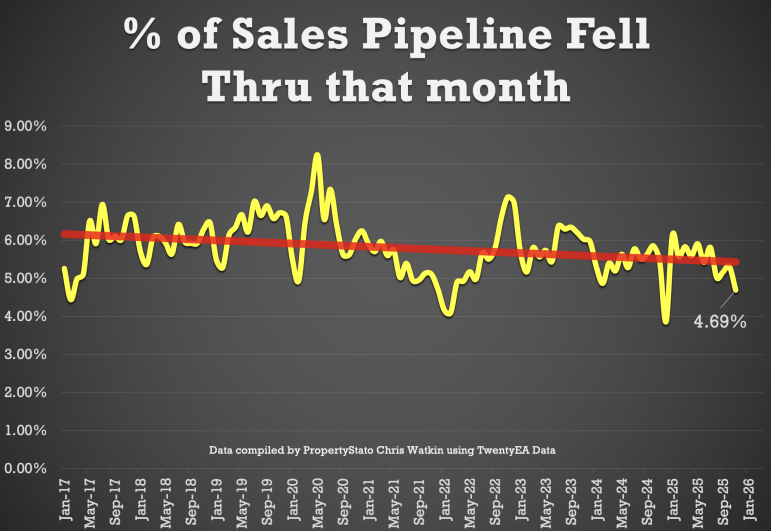

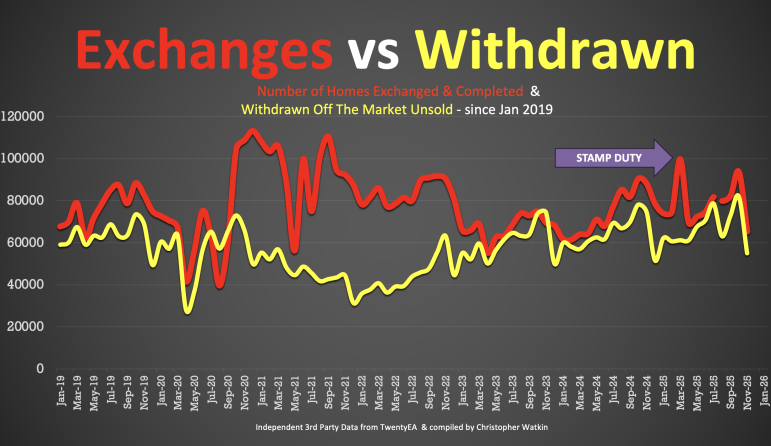

✅ Fall-Throughs

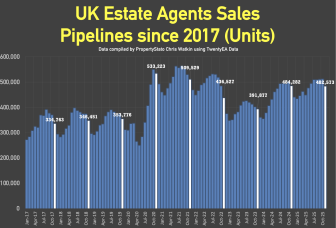

+ 4,783 fall-throughs final week (pipeline of 482k house Bought STC).

+ Weekly common for 2025: 6,100.

+ Fall-through charge: 25.8%, barely up from 24.9% final week.

+ Lengthy-term common: 24.2% (post-Truss chaos noticed ranges exceed 40%).

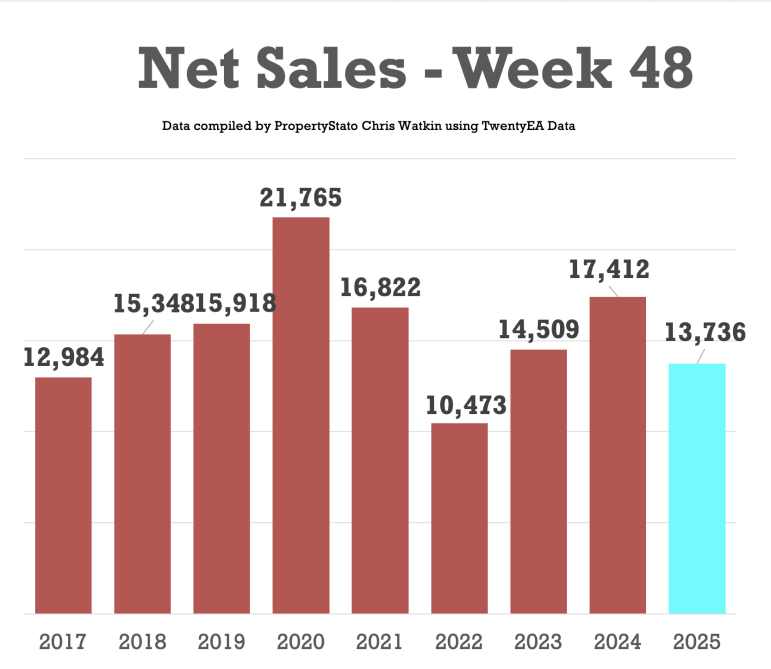

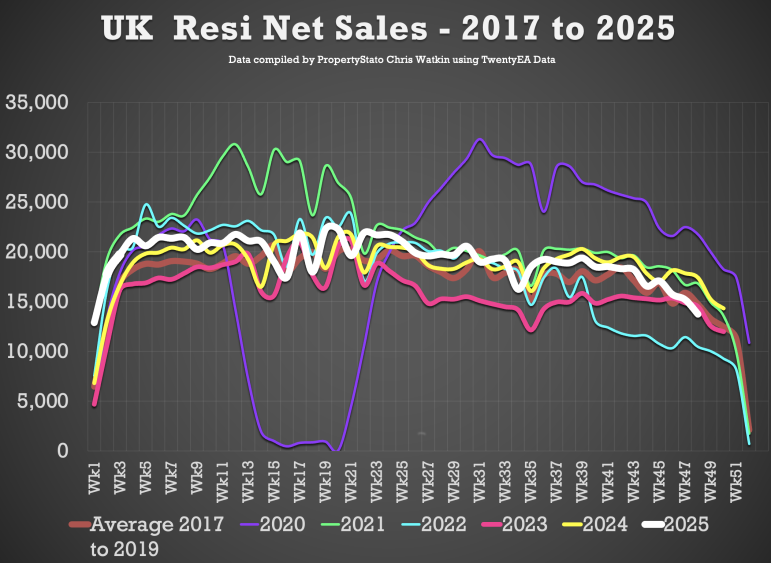

✅ Internet Gross sales

+ 13.7k web gross sales this week, down expectedly from 15.2k final week.

+ 9-year Week 48 common: 15.4k.

+ Weekly common for 2025: 19.3k.

+ YTD: 929k, which is 2.2% forward of 2024 (909k) and eight.6% above 2017–19 (855k).

✅ Likelihood of Promoting (% that Alternate vs withdrawal)

+ November Stats : 54.3% of properties that left brokers’ books exchanged & accomplished in November. (Notice this determine will change all through the month as extra November stats are available in). (65.3k exchanges & 55k withdrawals as at eighth Dec 2025)

+ October 53.3% / September: 53.1% / August :55.8% / July: 50.9% / June: 51.3% / Could: 51.7% / April: 53.2%.

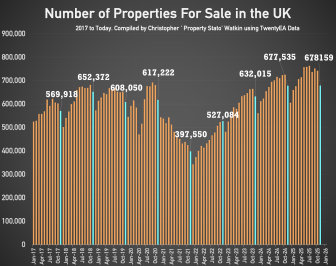

✅ Inventory Ranges

+ 678k properties in the marketplace on the first of December, down from 742k on 1st of November. December ’25 is an identical to December ’24.

+ 482k properties in gross sales pipeline on the first December, nearly an identical than 12 months in the past.

✅ Home Costs (£/sq.ft)

+ November 2025 agreed gross sales averaged £342.27 per sq.ft. 0.7% increased than 12 months in the past and 12.6% than 5 years in the past. The £/sqft at sale agreed matches the HM Land Registry Index with a 98% accuracy, 5 months upfront.

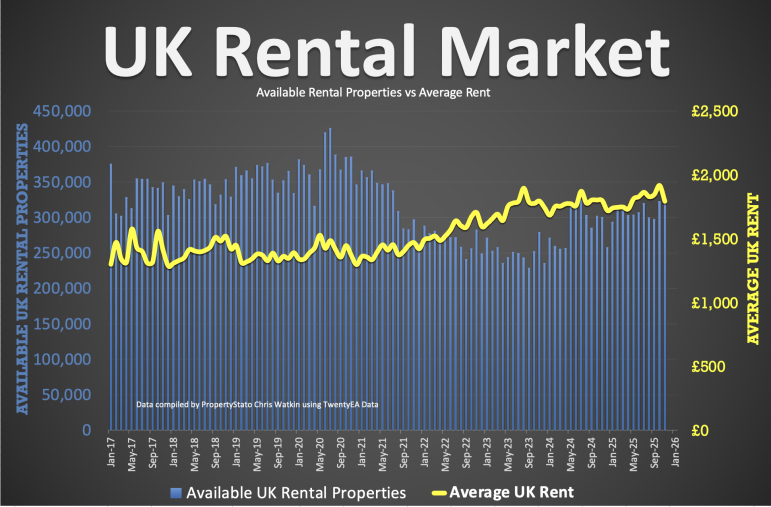

✅ UK Rental Market Overview

+ Common Lease in November – £1,791 pcm – a drop of 6.5% from October ’25 when it was £1,916 pcm. For extra comparability, Common hire was £1,785 in Nov 2024 and £1,557 in Oct 2017.

+ Accessible Rental Properties in November ’25 – 321k in comparison with 300k in November ’24.

+ Notable enhance of twenty-two.8% extra rental properties in Outer London than 12 months in the past, but a 3.7% lower in Internal London – Unsure why.